Exchange rates are ratios of the price of one currency to another. We should be careful about saying “the” exchange rate without being clear as to which particular ratio we mean and why.

*

Exchange rates often dominate the financial news. In 2016 the Chinese exchange rate has been frequently mentioned as a source of concern. But what does the exchange rate actually mean?

An exchange rate is a price or ratio. All prices are ratios, expressing the conversion of something into units of currency. A loaf of bread costs a pound, which is a price expressed in terms of sterling currency. The sterling currency itself has a price, expressed in terms of its cost relative to another currency. So an exchange rate is the price of one currency relative to another.

This means there is an exchange rate for every pair of currencies: pound/dollar, euro/dollar, yuan/dollar etc. Yet we often hear of “the” exchange rate. In practice some exchange ratios are more important than others, because a large volume of trade or financial transactions is conducted in that particular pair. But it can be misleading to single out one exchange rate pair.

The yuan/dollar rate

The rate that is most often quoted in connection with China is the yuan/dollar rate. (Note that China’s currency is called the RMB, which stands for people’s currency, and is denominated in yuan; the equivalent is that the UK currency is called sterling and is denominated in pounds).

For several years the yuan was gradually appreciating against the dollar, though not fast enough for many US politicians. That trend reversed in 2014, mainly because the dollar started strengthening against most other currencies, not just the yuan, reflecting the relatively strong growth of the US economy and the accompanying expectation (made fact in December 2015) of rising US interest rates.

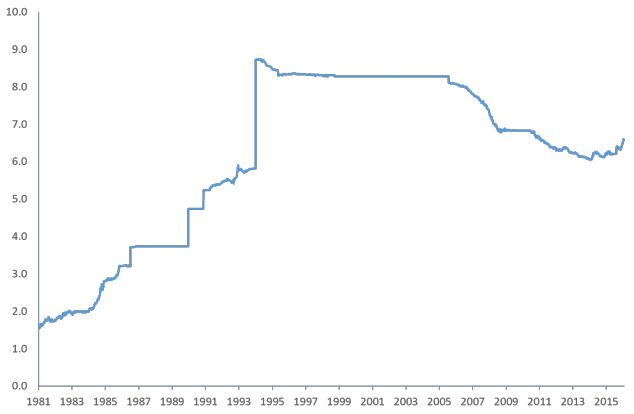

Many Chinese seem particularly interested in the yuan/dollar exchange rate. In December in Shanghai I was surprised to hear several people sounding anxious about a future fall in the value of RMB versus the dollar. They were talking about putting some of their money into dollars before this happened. Here is a chart of the yuan/dollar exchange rate, plotted conventionally to show the number of yuan per dollar. That means a rise in the line (more yuan per dollar) indicates a fall in the value of the Chinese currency versus the dollar.

You can see that in the 1980s, before the Chinese economy was opened up to international trade, the yuan was fixed at an artificially high rate to the dollar (1.5/dollar). By the mid-1990s the rate had been allowed to fall to something much more consistent with the economic relationship between China and the US. The Chinese central bank (the People’s Bank of China – PBOC) then adopted a fixed exchange rate policy in which the dollar/yuan rate was held pretty rigidly at about 8.3 yuan per dollar. This policy came under attack from the US for holding the value down (making Chinese exports artificially competitive in the US). China began a policy of allowing slow but steady appreciation of the yuan from 2005 and the value rose from 8.3 to 6 yuan per dollar by early 2014. But the line then reverses direction again, showing that the yuan started to fall in value against the dollar.

This reversal was caused by a rise in the dollar, which appreciated against all other exchange rates. But concerns that the slowdown in the Chinese economy were leading the PBOC to allow or even encourage a further fall in the yuan exchange rate were behind the worries of my Chinese friends in Shanghai. The value of the yuan against other currencies is not falling. It is inevitable that if the US dollar is strengthening in general then it will rise against the yuan. That is a dollar phenomenon, not a yuan one.

The new RMB basket

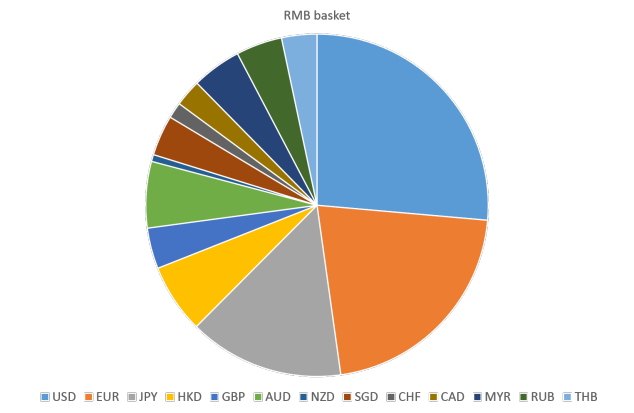

Unfortunately the exact policy of the Chinese central bank on the exchange rate has not always been clear. But it was widely believed to be targeting the yuan/dollar rate in the past. But recently it seems to have shifted to targeting the yuan against an index of currencies, of which the dollar is only one. That index was published in December 2015 on the website of the China Foreign Exchange Trade System (a subsidiary of the PBOC). The dollar has a weighting of 26%, large but much less than 100%. The composition of the index is intended to capture China’s weighted average of trade. Here is the full index composition:

(The colours refer to US dollar, euro, Japanese yen, Hong Kong dollar, Great Britain pound, Australian dollar, New Zealand dollar, Singapore dollar, Swiss franc, Canadian dollar, Russian ruble and Thai baht).

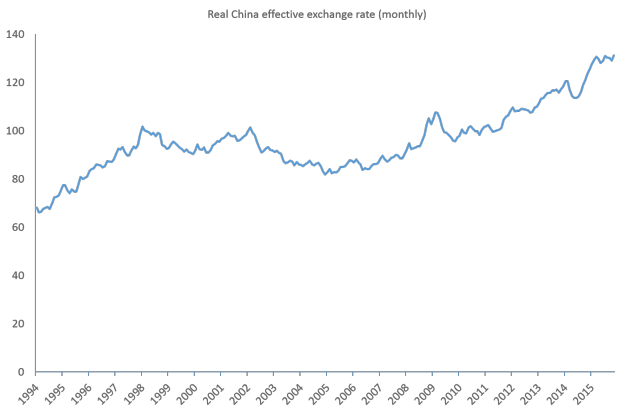

So in future, markets need to consider not just the yuan/dollar rate but the broader yuan index. It’s quite possible for these to move in opposite directions. If we look at the historic development of China’s exchange rate against a basket of currencies, it looks a bit different from the earlier chart against the dollar alone. This is the real effective index of the Chinese yuan as calculated monthly by the Federal Reserve (it’s only available back to 1994).

This index captures the value of the yuan against China’s main trading partners (“effective”), of which the US is just one. It also adjusts for inflation (hence “real”). The result is expressed as an index, since this is a combination of several different pairs of exchange rates. It shows that the yuan has been broadly trending upwards in the last ten years, including in 2015. It confirms that the Chinese overall exchange rate has been rising (most of the time) and that the fall against the dollar is a by-product of dollar strengthening.

Conclusion

China’s exchange rate policy hasn’t always been made very clear, which has contributed to market anxieties. But the broad message seems clear: the yuan has not been weakening in recent years, except against the dollar.

shahid saleem

Dear Sir,

What is your view on probability & scope of this scenario:

“Yuan’s possible depreciation actually happens during 2016 but against only one currency i.e, US dollars due to heavy dollar outflows, strengthening dollar or US internal economic reasons, same may have diluted affect on Yuan vs. Basket. Will same create chances of inter-bank triangular arbitrage, provided other banks go with 100% free float”