There are two generic ways in which a company can raise long term funding, which we call capital: debt and equity. Combinations of these, called hybrid capital, are also possible but rare outside venture capital.

Any economic agent, including individuals, companies, governments and charities, can raise debt (if they can find somebody willing to lend to them). But only a company or corporation (these are equivalent terms) can raise equity.

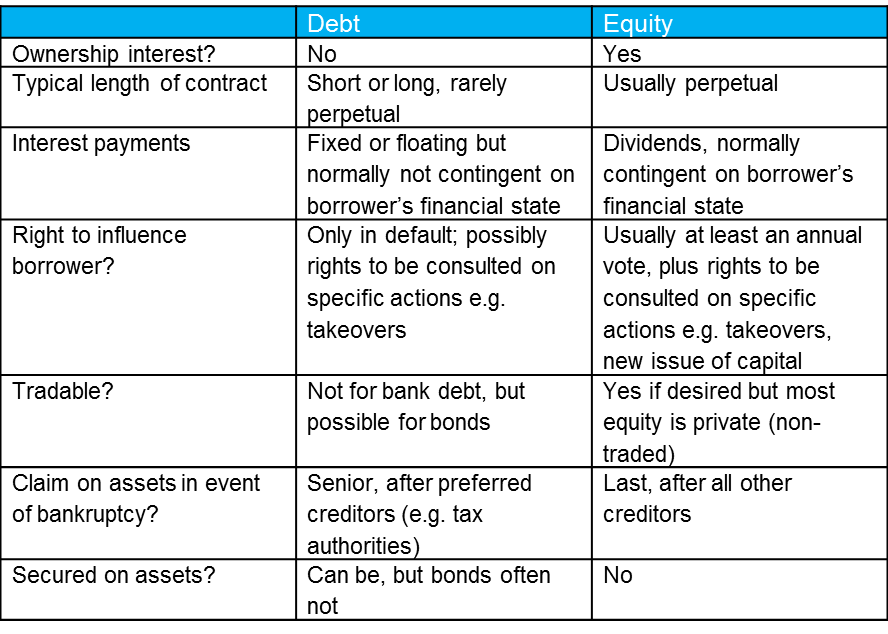

Figure 1 shows the main features of debt and equity

Figure 1 Debt versus Equity Finance

A debt contract is one in which the lender agrees to provide funds to a borrower who undertakes to repay them at a certain point in time and where there are periodic interest payments. So long as the borrower makes the contracted payments, she is free to do what she wants with the business and its assets.

An equity contract requires the borrower to make payments out of profits to the lender (“shareholder”) as and when that is possible, and economically desirable (sometimes the shareholder would prefer profits to be reinvested in the business, to maximise its future value, meaning fewer dividends today but more in future, if all goes well). This entails a degree of trust and of risk for the shareholder, who is compensated by having a share of the ownership of the business. So if the borrower appears incompetent or dishonest, the shareholder can appoint a new manager for the business and make any other changes that seem sensible. The problem for the shareholder is knowing what the borrower is actually doing with the funds.

Length of contract

The length of an equity relationship is typically perpetual, because most businesses are set up with the intention of living indefinitely. Occasionally a project may be terminated short of bankruptcy such as a gold mine that has become exhausted, or a franchise or other operating contract of fixed length. Even then the equity deal would normally be perpetual but provide for the liquidation of the firm if there was no possibility of continuing.

Debt contracts are nearly always of fixed length. It is precisely the relative certainty of the term of principal and interest payments that makes debt attractive. Of course the payments may stop owing to a problem of creditworthiness but that is an easier thing to assess than the ability in an equity contract to pay dividends (see below).

Short term debt (up to one year) provides for the working capital needs of a business or government and for relatively small loans for a consumer (to fund a holiday say). Short term debt can be provided by banks, in the form of an overdraft to a business or unsecured consumer loan. Or it can be provided through a range of securities-market based products, known as the money markets. Short term debt securities are often known as bills.

There is no equivalent of short term equity, though it is possible that an equity investment has a very short duration. For example an equity investment in a company that is then suddenly subject to a successful takeover bid could lead to the shareholder getting their funds back rather quickly. Equally an equity funded purchase of a building for speculative gain (perhaps to take advantage of a change of use clause that means it can be redeveloped profitably) may be short term. But the contract itself is usually perpetual. It is simply that the change of circumstances leads to the equity being repaid quickly.

Longer term debt securities (more than a year) are known as bonds.

The payment received: interest versus dividends

A loan is usually accompanied by interest payments. A standard debt contract consists of an amount to be lent (the principal), the date when the principal is to be repaid and the interest payable by the borrower to the lender. This usually takes the form of an annual fee (which can be paid quarterly or every six months), calculated as an effective interest rate.

For a bond, the interest is usually paid every six months and is known as the coupon. The coupon is a fixed amount of money. The effective interest rate is the ratio of the coupon to the principal, with appropriate adjustments for the time value of money.

The only reason we say “usually” is that it is possible for the interest payment to be paid at maturity together with the return of principal. For a short term loan this may take the form of a discounted loan: the lender lends say $100 but only provides $90 to the borrower, who nonetheless has to repay the full $100. The extra $10 represents the interest on the loan. This arrangement is normal on the short term debt securities called bills, issued by governments (Treasury bills) and companies (commercial bills). It simplifies ownership because there is no need to record who owns the bill, which can therefore very easily be sold to someone else. Whoever owns it on the date of maturity can claim the $100 from the borrower.

Longer term securities can be paid without interim interest also, in which case they are known as zero coupon bonds. Such a security might appeal to somebody who pays tax on the interest but not on capital gains. So if they buy a bond for $80 and get $100 back two years later, they receive no coupon interest but a $20 capital gain. Assuming this is exactly equivalent in value to the stream of coupons that another bond would pay, then the investor gains by not having to pay tax. Advanced financial markets allow conventional bond securities to be divided synthetically (“stripped”) into a stream of interest payments and zero coupon bonds, to allow the maximum flexibility in creating patterns of cashflows that suit the various customers.

Right to influence the borrower

An equity contract, which brings an ownership interest, entitles the equity investor to the normal rights of ownership, though these can be modified in a shareholder agreement that might regulate the voting and other conditions under which shareholders influence the business that has taken on the equity finance. But in principle the shareholder has a right to influence the company. Companies are usually required to have at least two directors, who represent shareholders, and to publish annual accounts. There should be an annual general meeting at which shareholders can vote and express views on the company’s activities and the composition of the board.

Debt lenders typically have no such rights other than what is agreed at the time of the loan. Any such conditions of the loan are described as covenants, which are legal promises to do, or not to do, things which might be affect the ability of the borrower to service and repay the loan. For example there might be a covenant that the company will maintain interest cover (profits before interest as a multiple of interest payments) at a minimum level of three times. If the covenant is “breached” then the lender can take control of the company or at least of its assets. But the debt holder cannot influence the borrower in normal times beyond what is mentioned in the covenants.

Tradability provides liquidity

When debt or equity is provided in the form of securities then it is relatively easy to sell these to a new owner. That might still be relatively cumbersome or slow if the securities are not listed on an exchange or traded over the counter (OTC). Trading brings greater ease of transfer of ownership, which makes the securities more liquid and therefore more valuable.

Bank loans are not normally traded but there is some scope for a secondary market for bank loans, meaning that the loan and all contractual rights attached to it are transferred to a new lender, for an agreed price. A bank that finds that it has excessive exposure to the steel sector for example, might want to sell some of its steel company loans. But the problem is that the borrower might see this as both a negative message about the state of their company and as a statement by the bank that it no longer wants to deal with the company in any area of financial services. Given the importance of relationships in finance, this would be potentially costly to the bank, so selling on a loan is not common, except very early in its life when the bank is merely initiating the loan and fully intending to sell part of it on to third parties, with the full knowledge of the borrower.

Luckily for banks which have changed their minds about a loan, the creation of credit derivatives in the 1990s allows them to sell the economic exposure of the loan without formally ending the legal or relationship part. A credit derivative called a credit default swap allows a bank (or any other lender) to in effect buy insurance against the loan defaulting. By neutralising the credit risk, for a fee, the bank can change the economic structure of its lending portfolio without upsetting any of the borrowers.

Claim on assets in the event of default

An important difference between debt and equity contracts arises in the event that the borrower is in default – unable to repay either the interest or the debt. In that case the debt lenders take control of the company and can decide whether to sell the company, liquidate its assets (sell what the company owns for whatever it can get) or restructure it to make it viable, but at the expense of the shareholders.

In these situations the shareholders’ interests come last. That is one of the risks that equity investors need to be compensated for. There may not be enough assets in a financially distressed company to repay the creditors, including debt investors, and the shareholders.

Is the funding secured on assets?

Loans are sometimes secured on a particular asset or group of assets, known as collateral. That makes the loan less risky because in the event of the company running out of funds, then those assets are ring-fenced from any wider liquidation process. The lender may claim them and sell them for whatever she can get, and keep the funds raised up to the point of the loan owing. To be suitable as collateral, assets need to be easily identified, hard to steal or damage and have a reasonably clear resale value. Land is the main form of collateral and mortgages – loans secured on property – are the most common form of secured debt. But intangible assets can in principle act as security, such as the rights to future music royalties, or other well defined intellectual property.

Loans can also be secured by a “general charge” on assets, meaning that no specific asset is nominated but the lender has first right to sell those assets to ensure payment, before other creditors are paid.

Equity cannot in general be secured. It is in the nature of equity to take whatever residual value remains after other creditors have been paid. Equity has the residual claim on all other cashflows or assets remaining, which in the case of a successful company could be a lot more than the assets used for securing loans. But in a failed or bankrupt company, there may be nothing left for equity providers once the assets have been sold to pay off the lenders.

Peter

Dear Simon

Presumably, a debt-for-equity swap does not require the consent or approval of equity shareholders following a chapter 11 and debtor-in-possession credit agreement (DIP)?

I`m thinking of the Cineworld C11 which is on-going atow. Lenders advanced a further $1.93B; presumably they want some sort of equity as compensation for the write off of the remainder of the debt ($5B)?

However the DIP appears silent on this – although heavily redacted.

Regards

Peter

Simon Taylor

I don’t know the details of the Cineworld case but in general a debt-for-equity swap reflects a situation where a company needs to strengthen its balance sheet (ie more equity), usually in some kind of distress or urgency. From the point of view of the existing equity shareholders this is bad news to the extent that it dilutes their ownership of the company, but good news if it preserves some of the value of the equity because the company remains a going concern. But the key decisions are taken by the debt holders, who compare liquidating the company with having their debt claims turned into equity, and decide what makes most financial sense to them. Equity shareholders lose most or all of their power once a company enters a chapter 11 or equivalent bankruptcy process.