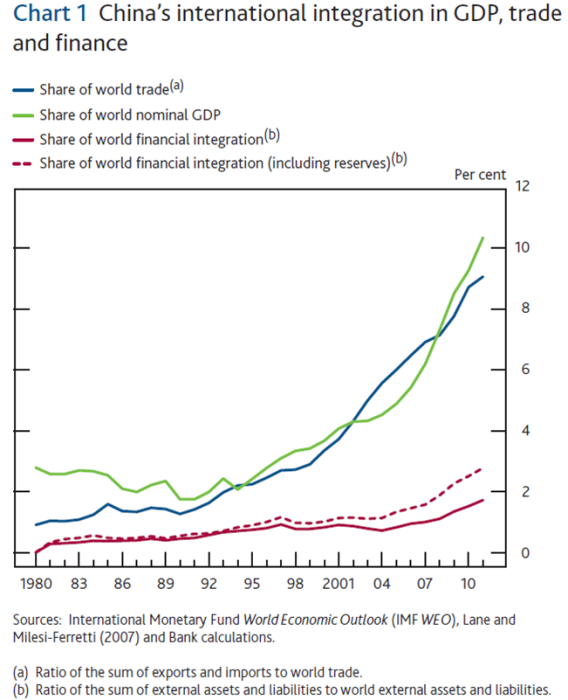

Perhaps a little lost in the Christmas shopping rush was an interesting article in the 2013 Q4 Bank of England Quarterly Bulletin about what might happen when China finally abolishes all controls on its international capital flows, consistent with its stated policy goals. China has already had a very large impact on the international financial system because of its foreign exchange reserves, which are by far the largest in history. But China’s overall financial assets and liabilities are much lower than those of the US, since the latter is much richer and far more financially developed economy. The first chart shows that China’s trade integration into the world economy has gone much further than its financial integration.

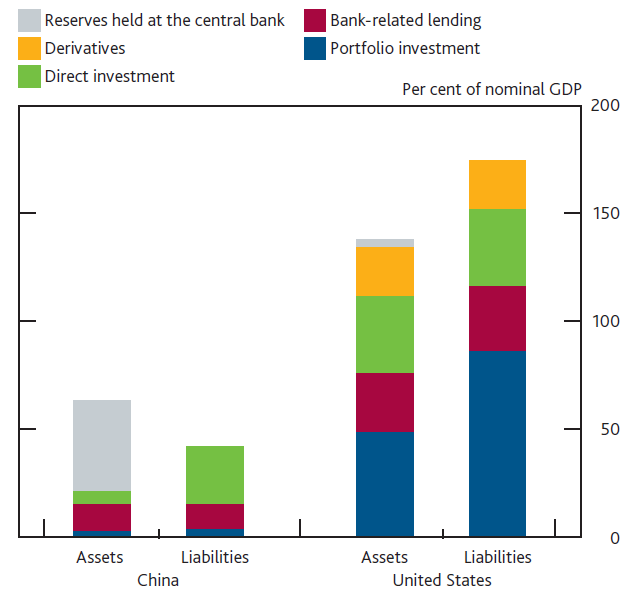

The second chart shows the scale of financial assets and liabilities now, for China and the US, as a percentage of each country’s GDP.

The US isn’t necessarily a goal or role model here. The high level of “financialisation” of the economy might be seen as a weakness or problem. But to some extent it’s natural that an economy of high average incomes will have a high level of financial services, which will show up as a high level of financial assets and liabilities. Middle class people want mortgages, car loans, life insurance, credit cards and pensions. Companies in richer economies want risk management, loans, bonds and equity finance. That’s why the growth of financial services in the less developed economies will be much faster in the next decade than in mature, rich economies where these things already exist.

The chart shows that China has virtually no derivatives assets at present but that is likely to change quite quickly as the government introduces bond futures and other basic derivatives. Note also the very high proportion of China’s financial assets which are held as foreign reserves by the central bank, the People’s Bank of China. The US holds a much lower volume of reserves, as it doesn’t try to manage the dollar exchange rate. (The US also has large holdings of gold, which have a reserve-like quality though they are not much use for stabilising an exchange rate in a crisis).

The Bank then tries to forecast the increase in China’s financial assets and liabilities that would follow opening up the country’s balance of payments capital account, which is the same as the “internationalisation” of the RMB as the policy is widely known. The third chart shows the enormous increase in China’s external assets and liabilities forecast by the Bank for 2025. From around four per cent of world GDP in 2012, the figure is forecast to rise to around a third of global GDP. On this view China will be a very large player in the international financial system in the near future.

There are three mechanisms by which the increase is forecast to happen.

1. Declining “home” bias. All countries show a degree of home bias, meaning that domestic investors allocate a higher proportion of their wealth to domestic assets than is consistent with entirely rational portfolio optimisation. Given the current capital controls blocking most Chinese from (legally) investing abroad, the current bias is nearly total and if China moves in future to a “normal” level of home bias, there would be a large expected outflow of investment abroad. Other countries too are expected to see a fall in home bias, which increased after the global financial crisis.

2. Catch-up growth. China is likely to grow at a faster rate than the rest of the world economy and much faster than the developed economies for some time to come, even if it decelerates from the 10% growth of the last 30 years. This will naturally lead to a growth of financial assets, much of them held abroad.

3. Closing the openness gap. The largest driver of the expected increase in China’s international financial assets and liabilities is the expected increase in external investment by and into China, from the current relatively low levels owing to capital controls. It is perfectly sensible for Chinese residents to want to hold some foreign assets, to diversify their portfolios. This could be foreign equities and bonds, perhaps through mutual funds, as well as real estate and direct investment by Chinese companies, which is currently very low but likely to grow rapidly. Foreigners will equally want to invest in what by then could be the world’s biggest economy. Currently direct investment by companies into China is relatively easy but foreign ownership of Chinese equities and bonds is only just being permitted (with the recent launch of ETFs allowing a modest amount of foreign investment in Chinese equity markets).

The Bank scenarios assume no interruption to the policy of liberalising the capital account and the associated major changes in the Chinese economy. This is not to be taken for granted. The re-orientation of the Chinese economy towards the market and away from the state is opposed by many elite insiders who have gained enormous wealth during the last couple of decades. Michael Pettis, a professor at Peking University, is a well informed and articulate writer of a blog arguing the view that successful reform is politically contentious and will inevitably lead to lower GDP growth in the next few years. A recent book Stumbling Giant by Timothy Beardson, who is an investment banker and long time Hong Kong resident, puts a broader dampener on China optimism, pointing out the bewildering range of challenges the country faces. A more optimistic view, also well argued, can be found in the book Eclipse, by Peterson Institute of International Economics author Arvind Subramanian.

So the Bank of England numbers only illustrate what could happen. But what a picture they paint.

Leave a Reply