A recent speaker on the MFin mentioned, almost in passing, that he didn’t think the Basel III regulatory system would actually be implemented, so flawed was its approach. I thought this sounded a little exaggerated but a recent speech from the the Vice Chairman of the Federal Deposit Insurance Commission (FDIC), Thomas Hoenig, suggests our speaker was on to something. Hoenig’s speech is titled “Basel III Capital: A Well-Intended Illusion”. It adds another well informed and intelligent critique of the use by Basel III (and Basel II) of “risk-weighted assets” (RWAs) as a measure of bank balance sheet strength. Other critiques include that of Bank of England Deputy Governor Andy Haldane and the recent, very readable book by Stanford economist Anat Admati and Bonn University economist Martin Hellwig”The Bankers’ New Clothes.

The argument made by all three sets of authors but most simply and clearly by Hoenig is that the Basel III measure of bank balance sheet strength is conceptually flawed and has been a poor predictor of bank failure. It would be better to revert to the simpler, cruder but more reliable measure of bank leverage. What do these terms mean?

Why balance sheet strength matters

All companies care about their balance sheet strength because if they fail there are significant costs to shareholders and other stakeholders. In the case of banks the taxpayer also cares because banks may require bailing out, or their failure can cause macroeconomic disruption. So while it may be somewhat academic as to whether Apple’s completely unlevered (debt-free) balance sheet is optimal for its shareholders, we all have an interest in whether the larger banks are properly capitalised, that is whether they have enough shareholders equity to cover plausible losses in a financial crisis, without needing government help.

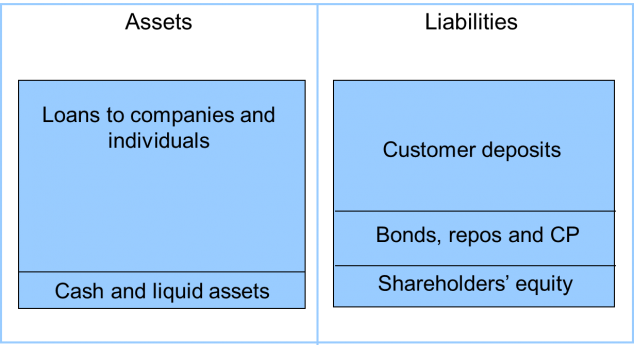

The standard measure of risk for any balance sheet is the leverage (or gearing) ratio. This is the amount of assets the company owns relative to it equity capital. This diagram shows a simplified bank balance sheet. The bank’s sources of funds are its customer deposits, plus funding from the capital markets in the form of bonds issued plus commercial paper and repos, which are both forms of short term funding from outside investors (*). Lastly the bank’s sources include the equity capital from its shareholders. Together these liabilities and equity are deployed by the bank in the form of lending to households and companies, with some funds kept in liquid assets such as cash in the vault and high grade securities that can be sold at short notice to realise more cash if customers want to take their deposits out.

Losses in assets automatically lead to a loss of equity (because the value of the company to its owners is reduced) and if there is not enough equity to absorb the losses then the company is insolvent. Leaving aside some moderately technical issues about what exactly is equity, the normal measure would be total assets divided by tangible equity (intangible assets and the equity they represent are usually excluded as the value of these assets is more difficult to assess and to sell for cash). This relationship can be expressed either as a multiple of equity or as a percentage of assets. So a bank with equity of 3% of assets is 33.3 times levered.

Basel and risk weightings

The Basel II and III approaches don’t use simple leverage, they instead use the ratio of risk-weighted assets to tier 1 capital, which is now the same as tangible equity capital, though in the past some other categories of capital were included. So the difference between the ratios is in the risk adjustment. Risk-weighted assets on the Basel definition are around only half of total unadjusted assets, for the major banks, according to Hoenig.

The concept of risk adjusting, like so many ultimately dangerous ideas in finance, started with good intentions. Not all assets held by banks have the same risk. So requiring them to own the same amount of equity capital against assets of different risk seems inefficient. For example mortgages and US government bonds are (or at least used to be) very low risk assets. Unsecured leveraged loans to companies are much higher risk. From this reasonable idea arose the whole RWA approach. Two problems then gradually became clear.

First, banks started using the risk weights to manage their balance sheets. They loaded up on lower risk assets and in doing so some of those assets became less safe, the most infamous example being the AAA-rated securities that were backed by collateralised debt obligations (CDOs), which in turn were vehicles for owning mortgage backed securities. The failure of the rating agencies accurately to capture the risks in these securities turned out to be a systemic flaw in the US banking system, which then became an international flaw when those CDO securities were sold round the world.

Second, risk weights change over time. Sovereign debt was zero rated in the Basel II scheme but we now know that some of that debt was very risky and led to actual write offs in the case of Greece, one of the things which wrecked the Cyprus banks. Many European banks bought lots of peripheral European sovereign debt because it was rated as equivalently low risk to that of Germany but paid a slightly lower interest rate, and even a few basis points of extra yield makes that worth doing.

The upshot was that banks with apparently strong Basel II balance sheets were woefully under-capitalised when the full sub-prime crisis hit. What is disturbing now is that banks which have respectable or even quite good ratios under Basel III still look very weak on the cruder but less easily manipulated leverage ratio.

Hoenig gives data for all of the G-SIFIs – the gobal systemically important financial institutions. I’ll choose a couple of banks for illustration.

How leveraged is JPMorgan Chase?

JPMorgan Chase is among the largest banks in the world and the most dominant in the derivative markets. It also did a better job of coming through the financial crisis fairly unscathed. And it convinced many people that it was the best-in-class for risk management. This may indeed be true but the failures associated with the bank’s chief investment office last year (the so called “Whale” trades that cost the bank around $6 billion) have caused that crown to slip a little.

On the Basel III risk-weighted basis, JPMC’s leverage ratio was 12.6%. That’s equivalent to saying that each dollar of equity capital supported about $8 of assets. The bank would need to lose 12.6% of its assets for the capital to be fully wiped out. That sounds reasonably reassuring, though we know that some assets can lose much more of their value than that in a difficult market (gold prices fell 9% in one afternoon recently, though that’s a little unusual).

But on the more conservative non-adjusted assets basis, the simple leverage ratio of assets to tangible equity, JPMC’s leverage ratio was 5.9%. That’s a lot less reassuring. It is surely not that difficult to imagine another crisis in which the bank’s assets fall in value by just 5.9%

But it gets worse. That 5.9% figure is based on US GAAP (generally accepted accounting principles). If you apply IFRS (International Financial Reporting Standards), the system used by most banks in the rich countries except in the US and Japan, JPMC’s leverage ratio falls to an estimated 3.5%. There is reasonable room for disagreement about the GAAP/IFRS approaches but as Admati and Hellwig point out in their book, the GAAP approach assumes that you can net off many of the derivative assets and liabilities, an assumption that was not consistent with what happened in the break down of markets in 2008. (The US was supposed to be joining up with IFRS until last summer when the project fell apart. I don’t know if bank lobbying had anything to do with this.) But if IFRS is more nearly correct, then JPMC need lose only 3.5% of its assets to become insolvent. This is not the “fortress balance sheet” we thought the bank had.

Two other examples. Morgan Stanley has a secure sounding 17.7% Basel III figure but that shrinks to 5.8% simple leverage (US GAAP) or 2.6% (IFRS). And most remarkably, Deutsche Bank’s 14.3% Basel III figure conceals a basic leverage ratio of only 1.5% under IFRS. Just to emphasise, that means that if Deutsche Bank lost just 1.5% of its assets it would be bankrupt.

No wonder the FDIC is concerned.

*

(*) Traditionally commercial banks were funded almost entirely from customer deposits and shareholders equity. But modern banks use many other sources of funding. Long term bonds are a quite good, stable source of funding because their long maturity matches the maturity of the bank’s loans. If, as is sometimes the case, the bonds are convertible into equity when the balance sheet is stretched, so much the better. Commercial paper is a form of short term security that taps the money markets, including the very substantial money market mutual funds in the US. Repos are short term, sometimes overnight, financing agreements equivalent to secured loans, where a bank sells a security such as a government bond to a third party with a promise to buy it back at a later date, the fee representing a de facto interest payment. Both CP and repo funding became highly unreliable during the financial crisis and several banks got into trouble because they couldn’t refinance their balance sheets. This was a financing problem, quite separate from the question of whether they had made poor lending decisions, which of course many had also done. Relying more on equity capital financing and less on short term funding makes a bank safer in two ways. First, it reduces the risk of short term funding drying up which can force a bank to make fire-sale asset disposals. Second it provides more loss capacity in the event of assets going bad for any reason.

UPDATE October 2013

Simon Johnson of MIT writes in the New York Times on too big to fail here.

A conference on the subject, including papers cited by Johnson, held at NYU Stern October 8 2013, details and slides here.

Can

Perfect Analysis! Thank you for sharing Simon! I dont know whether I am right but I guess banks dont want to raise additional Equity Capital because this will dilute their existing shareholders and decrease the ROE metrics. So instead of raising new Equity capital to strengthen their capital bases and increase overall (E/RWA), they now, instead, choose to tighten lending and other relatively riskier activities so that they can manipulate the RWAs. After all, if you dont want to manipulate numerator, you can always change the denominator to get to where you want. So I believe this is another reason why we dont have much lending activities. This is also matched with cost cutting measures in order to offset the overall reduction in profitability in margins and increase the ROE again.

william

That is an interesting piece! The guardian reported on 26 February 2013, that it had become clear after the banking crisis that banks have been too smart for their regulators and it seems this is still the case. This follows a survey conducted by Europe’s top banking regulators finding discrepancies in ways banks measure risk weighted assets with impact on the amount of capital they need to hold.

The European Banking Authority (EBA) concluded that there were material differences in the way risks are measured across 89 banks in 16 countries across the European Union. Other regulators around the world are facing similar challenges and we wonder how fairly capitalised the banks truly are.

Fran

I hope that the newly published Basel III reform package, including the imposing of 3% minimum leverage ratio plus associated buffer, will help alleviate some of the concerns.