Latest data show that the US dollar remains the dominant trading currency globally, and is still the pre-eminent foreign reserve currency, though slowly losing ground, mainly to other developed country currencies.

*

Perhaps the question I have been asked most over my years as a finance teacher is whether the dollar is about to lose its global role. My answer has always been: not yet and probably not for some time. My latest answer, based on the latest data, remains the same, but with the caveat that confidence in the US dollar as a safe asset is in danger of erosion in the next decade.

There are two ways in which people refer to the dollar as a global currency: i) as the main counterpart in foreign exchange (FX) trading; and ii) as the main currency of use for foreign exchange reserves held by governments and central banks. These are somewhat related but distinct measures.

I The dollar as a trading currency

The Bank for International Settlement’s latest triennial survey of FX trading was published in December 2025 (preliminary data, which are not very different, were published in September). Key findings include:

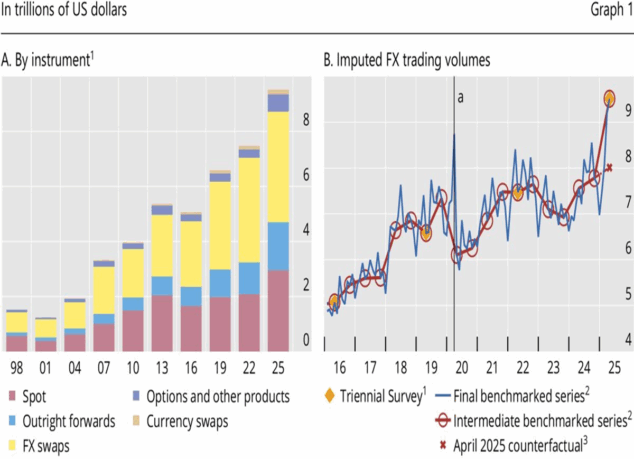

1. Global FX trading continued to grow, reaching $9.5 trillion daily in April 2025 (22% above the previous survey figure for April 2022). This is about 30 times global GDP and 70 times global trade. The 2025 level was boosted by unusual levels of hedging around “policy uncertainty” as the BIS diplomatically puts it, as well as growth in the so-called Treasury Bond cash-futures basis trade, in which hedge funds buy T-bonds, using a lot of leverage (in the repo market) and buy the equivalent T-bond future, for a small gross interest return, magnified by the leverage (*). Figure 1 shows the overall historic growth, including the BIS’s estimate of the “counterfactual” level of trading in April 2025, adjusting for the temporary surge in dollar hedging.

Figure 1 Global foreign exchange trading volumes hit new record

Source: BIS Quarterly Review, December 2025

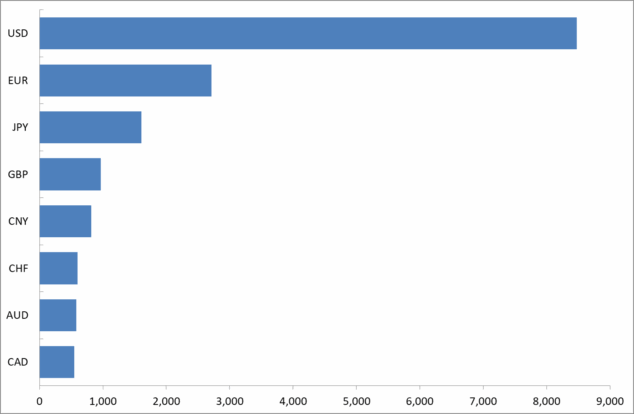

2. The US dollar continues to dominate, being the counterparty in 90% of all FX trades. As figure 2 shows, the other main traded currencies are all developed economies, except for the offshore Chinese Yuan (CNY) which is gradually growing in importance, but lags far behind China’s role in international trade or GDP. This is mainly because the Yuan is largely an on-shore currency behind capital controls that stop it being more widely traded.

Most growth of the use in CNY is in trade with China. But the US dollar is used widely in transactions that don’t involve the dollar, because of its huge liquidity. Imagine someone wants to do business between say Chile and Poland. There is a market for such transactions but it’s much less liquid than the markets for Chilean pesos to the dollar and for Polish zlotys to the dollar. So it’s cheaper and easier to go from pesos to dollars and then dollars to zlotys. It is unlikely that the CNY could fulfil this role anytime soon.

Figure 2: Global FX trading still dominated by US dollar ($ billions)

Source: BIS; author’s estimates; CHF is Swiss Franc; AUD is Australian dollar; CAD is Canadian dollar.

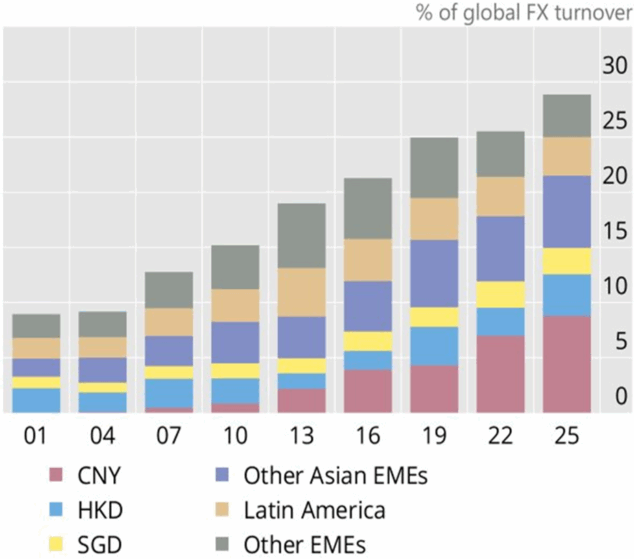

3. Growth in emerging market economy (EME) currency trading is growing, led by the Chinese Yuan (CNY). Let’s leave aside the oddity of describing China, the world’s largest manufacturer and largest exporter, and Singapore, one of the world’s richest and most developed economies, as emerging market economies. Figure 3 shows that EME currencies now account for nearly 30% of global turnover, led by CNY and by the Hong Kong dollar, which is a separate and fully convertible currency that is offshore with respect to the mainland Chinese economy.

Figure 3: CNY and HKD drove the increase in EME currencies’ share of global FX turnover

Source: BIS Quarterly Review, December 2025

II The dollar as a reserve currency

What about foreign exchange reserves? This refers to the currency in which governments or central banks hold their foreign exchange reserves. Like any reserves, these are financial assets held to protect against macroeconomic volatility or shocks that hit a country, where holding foreign assets allows the government to intervene to protect the currency.

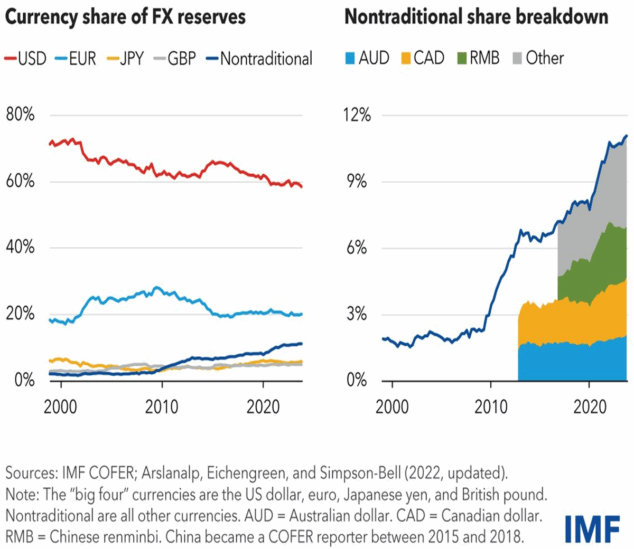

The IMF issued a blogpost in June 2024, co-authored by the distinguished international economist and economic historian Barry Eichengreen, which showed that the US dollar share has declined to about 60%, from about 73% in 2000. But the share has been lost mainly to other developed economy currencies such as the Australian and Canadian dollars. The Chinese Yuan share has also risen but only to just over 2%. (The latest IMF data for 2025 Q3 show a slight fall since then, but there are questions about whether China’s FX reserves are being disguised by being held by Chinese commercial banks, rather than by the central bank, the People’s Bank of China). Figure 4 shows the key trend from that blogpost.

Figure 4 US share of FX reserves is highest, but has been falling, replaced by “non-traditional” reserve currencies.

FX reserves need to be held in a large, liquid market where the assets can be sold quickly when needed. Since China’s main financial markets remain behind foreign exchange controls, they are not an ideal place for keeping FX reserves (this doesn’t apply to the HK dollar of course). Unless this changes, it’s unlikely that other countries will want to put too many of their FX reserves in Yuan.

III Conclusion: dollar dominance remains strong

The fact that the US dollar still dominates international finance should not be that surprising, as it’s mainly a result of lock-in, or incumbent advantage. Parts of the world were still using the pound sterling even in the 1960s, despite the UK having long since lost its economic dominance.

The threat to the dollar is largely in the US itself, especially the apparently remorseless growth of US federal government debt. Ken Rogoff, a highly distinguished macroeconomist and former chief economist at the IMF, is not somebody to jump to conclusions. But in his very readable book published in April 2025, Our Dollar, Your Problem: An Insider’s View of Seven Turbulent Decades of Global Finance, and the Road Ahead, he sounds quite concerned. In a postscript, written after the news that Donald Trump had been elected to a second term as US President, he writes:

One can hope for a long period of strong growth and low inflation, but it would be folly to ignore the many “this time is different Pax Dollar assumptions built into today’s markets that may well be upended over the next decade, if not much sooner. (p. 291)

***

(*) There is a short BIS video about this trade and the risks it contains here.

Leave a Reply