On 22 July 2025, the UK government announced that Sizewell C new nuclear power projects reached final investment decision (FID). A look at what has been announced contains some surprises and prompts questions. Comments and corrections are most welcome.

*

Sizewell C is a 3,200MW new nuclear power project, to build two twin European Pressurised Reactors (EPRs) next to the Sizewell B 1,200MW Westinghouse Pressurised Water Reactor (PWR) and the Sizewell A Magnox reactor which closed in 2006, on the Suffolk coast in the east of England. A copy of the identical twin EPR at Hinckley Point C project under construction in Somerset, on the west side of England, Sizewell C, by using the same construction and project management teams as Hinckley, promises quicker and cheaper construction. Despite that, the announced project funding runs to £50 billion, and appears to have a target cost of £38bn, which would make it one of the most expensive power stations ever built.

It is obvious to anyone living in east Suffolk that construction has already started (my cousin lives in Leiston, an economically depressed town close to Sizewell, which should benefit greatly from the project). An amateur pilot recently showed me aerial photos of huge areas of land having been cleared to make room for the project. Sizewell received full planning consent in July 2022, but a judicial review brought by objectors, was only rejected in June 2023. For reasons that are unclear, but are partly owing to the change of government in 2024, only in July of 2025 did the government release the financial terms of the project.

Key facts (*)

- Total financing £50bn of which £8.5bn equity and £41.6bn

- Target construction cost £38bn

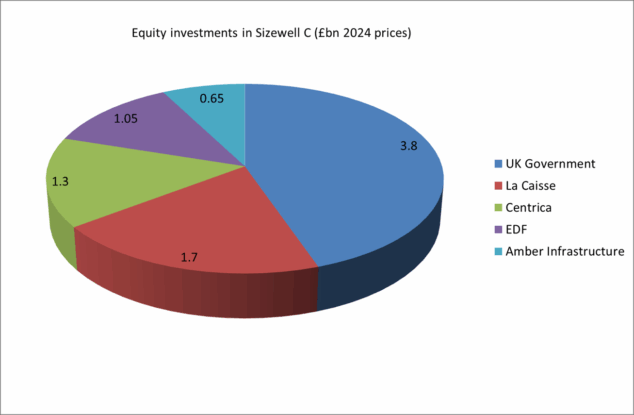

- Equity: UK government to invest 45% of equity (£3.8bn), the rest sourced from EDF (the French state-owned electricity group) and private investors

- Debt: A total of £41.6bn, of which £5bn to come from the French export credit agency (de facto the French state) and the rest from the UK’s new National Wealth Fund (previously the National Infrastructure Bank, set up and owned by, but operationally independent of the Treasury – so de facto UK state funding).

The equity shareholdings are summarised in chart 1. Note that £400m of the equity funding under Amber Infrastructure (a private international infrastructure manager), is coming from the Nuclear Liabilities Fund, a ring-fenced fund for the decommissioning of EDF Energy’s eight existing UK nuclear power stations.

Comments

Overall debt/equity ratio of 83% is relatively high. This is a little higher than the usual 70/30 debt/equity split for infrastructure projects. At the construction phase most projects would start out with even more equity, refinancing with more debt once the project has been built and is operating, when the risks are much lower. This ratio leaves little room for such refinancing in future.

All state-funded debt. When I and colleagues from the Energy Policy Research Group wrote about the overall regulated asset base (“RAB”) approach to nuclear funding in 2019, I did some cursory research into potential private sector investors. One clear message, even from a small sample, was strong appetite for long term, inflation-linked debt that could be issued by Sizewell C.

Inflation indexation is an inherent feature of the RAB (“regulated asset base”) model, which builds on existing UK network utility regulation, in which revenues are set relative to inflation for periods of typically five years. That allows such regulated companies to issue inflation-linked debt, since their revenues are inflation-linked. The UK market for inflation-linked debt is dominated by the UK government’s index-linked gilts (known as “linkers”) but yields are often thought to be depressed by the required buying by insurance companies to meet their regulatory obligations. There is a more limited, and not very liquid OTC (over-the counter) inflation swaps market (see this Bank of England working paper for more information), in which investors can buy inflation-protection separately. But having a large, long term and presumably creditworthy issuer of inflation-linked debt would have been welcome. The government has decided not to tap this market.

More generally the market for long term debt liabilities is underserved. There are some multi-decade loans out there (St Catharine’s College has a 45 year loan outstanding, among other Oxbridge colleges) but these are usually illiquid, bespoke deals with insurance companies. A new source of very long term corporate debt (assuming we treat Sizewell C as a corporate issuer) would have been welcome.

Most of the equity is from governments. With 45% of the equity coming from the UK government and 12% from the French government (via EDF), 57% of the project is state-owned. There is nothing magical about this, but it means we should be careful in describing this as a privately-funded project. Potential private investors told me that they wanted the UK government to have some “skin in the game” but that surely didn’t require such a large stake. I would guess that the long term plan is for the UK government to sell some or even all of its equity, once the project is built and operating.

Nuclear Liabilities Fund investment is interesting. The NLF is, in effect, a pension fund for retiring nuclear power stations, the idea being to build up a stock of assets during the stations’ operating lives sufficient to pay for all closure, defuelling and decommissioning costs, which will stretch some decades beyond the closure of the stations. Like any defined benefit pension fund, one would expect an asset allocation tilted towards growth assets such as equity. It’s not clear why investing in the private equity of an asset whose risks are somewhat correlated with the risks of the liabilities being funded is such a good idea.

The NLF has its own board of trustees, with their own legal responsibility for ensuring the fund meets its objectives. Three of them are appointed by the government and two by EDF. These trustees, and the directors of the NLF: “have regard to the interests of stakeholders. Stakeholders include DESNZ, EDF Energy, NDA [Nuclear Decomissioning Authority], UK taxpayers and the public at large.” It might be considered that there could be differences of interest between these stakeholders. But the trustees and directors would need to satisfy themselves that investing in the equity of Sizewell C would be consistent with the purposes of the fund. One explanation might be that NLF has a particularly long liability horizon (over a century till the final decommissioning costs fall due) and the fact that Sizewell C will be a very long-lived asset makes it a good fit. NLF can also take illiquidity risk, even more that most pension funds, so private equity is a justifiable investment.

National Wealth Fund is putting most of its financial firepower into Sizewell C. The NWF has £27.8bn “for transformational UK projects” according to its website. According to the Financial Times, the NWF debt for Sizewell C is separate from this and will be raised in the gilt (UK government bond) market. In which case, it’s not clear how it differs from direct government funding. Perhaps there is some accounting principle here which will keep the debt off the UK government balance sheet, but I doubt it. It means that Sizewell C will for the time being at least, rather dominate the financial activities of the NWF.

The target project construction cost is £38bn, including a contingency (again according to the Financial Times). The FT also reports that shareholders would receive a higher return if costs come in below £40bn in the sense that cost-savings would be added to the asset base on which they will receive a return. If costs exceed £47bn, private investors need not put in any more capital, implying that the UK government would fund any such cost over-runs. This de facto insurance against project over-runs is called the Government Support Package (GSP), described as “the government provision of support intended to cover against specific high impact, low probability (“HILP”) risks, that private investors would not be able or willing to finance themselves, either at all, or at a level which represents VfM [value for money]”.

Although it is conceptually distinct from the RAB remuneration model, the GSP is an essential part of the overall RAB financing approach, as used in the pioneering Thames Tideway Tunnel, which was completed in 2024. Without it, private investors would be fully exposed to the construction risk that has dogged new nuclear projects in Europe and the US in recent years. In that case they either wouldn’t invest at all, or would demand much higher rates of return.

Accounting cost of capital looks low. Using a conventional capital asset pricing model approach to the cost of capital , I estimate a weighted average cost of capital of about 4.7%. This assumes 80% debt, using the current 10 year gilt yield of 4.6%, which after 25% corporation tax is 3.5%. I’ve assumed a cost of equity of 9.6% (let’s call it about 10%, given the margin of error), based on an estimated equity risk premium of 5% and a beta of 1. It could be argued that the equity has been de-risked by the government’s Government Support Package but numbers quoted in the Financial Times suggest investors expect double digit internal rates of return, consistent with a beta of at least 1.

This 4.7% is the estimated return that would drive the remuneration allowed the regulator. It is an underestimate of the true cost of capital of the project. First, the cost of gilts is the marginal cost of government borrowing, not the actual credit risk of the project. It would be easy to justify all capital investment in the whole economy being financed by government borrowing on the grounds that it’s the cheapest form of finance, but apart from obvious operational concerns, this would be an illusory exercise. Second, the equity risk is reduced by the government’s contingent equity promise, the Government Support Package. The taxpayer is paying for this insurance, but the cost is not at all transparent. The government’s Value for Money analysis argues that: “Compared to the counterfactual of delivering alternative low carbon technologies, the results from the power system modelling suggest that building SZC reduces the cost of the power system and generates a positive return on government investment.” Of course in the happy case that construction costs come in on target, no extra government funding will be needed, but that doesn’t mean the promise to provide extra equity is free.

But crucially, the accounting cost of capital will drive the actual price of electricity that Sizewell C is paid, which I estimate very roughly in the region of £100/MWh (I hope to improve that estimate with further information). That compares with the 2025 Contract for Difference auction maximum for offshore wind of £113/MWh (in 2024 prices). Hinckley Point C’s contract specified £92.50/MWh in 2012 prices, falling to £89.50 if Sizewell C goes ahead, which is now the case. In 2025 prices that would be about £129/MWh. Nuclear is of course baseload electricity and more valuable than intermittent wind or solar. So the government could probably defend the Sizewell C number of £100 (if my estimate is at all accurate) compared with offshore wind, which is where most of the UK’s new power generation capacity will come from in the next decade.

Questions

I hope to learn more about the details and motivations of the Sizewell C project in due course. My main points of curiosity are:

Why is there not more private investor equity? Was it a lack of demand? Or just that the government wanted to dominate the equity side during construction?

Why did the government decide not to use any private debt? My guess is that it keeps the measured cost of debt down, as UK gilt rates are obviously below corporate rates. But the true cost of debt is higher than the marginal cost of government debt, if the project contains any credit risk, which it must do. By picking up this risk, the taxpayer is taking on risk but not being compensated for it.

Why use the NLF rather than normal UK government debt? Again, this is probably an accounting matter, but accounting can make things clearer or more obscure, according to circumstances. And what is the significance (if any) of the equity being owned by the government but the debt being provided by the NLF?

(*) Sourced from the official government site and the Financial Times.

NBA

The article provides a detailed look at the financial structure of the Sizewell C nuclear project, highlighting the complex interplay between government funding, private investment, and regulatory frameworks. It raises important questions about the true cost of capital and the role of government support in such large-scale projects.NBA