Oil and gas companies have few skills that are transferable to electricity generation and risk wasting a lot of their shareholders’ money.

*

“Peak oil” used to refer to supply but in recent years has come to mean the year when global oil demand peaks and then starts to fall. Few people now seriously dispute that oil demand will peak soon because of a shift to electric vehicles and more generally a reduction in fossil fuel use. Oil optimists see a long term need for oil in the manufacture of plastics but even there the outlook is uncertain.

This is all good, because we urgently need to curb greenhouse gas emissions. Oil and gas companies have increasingly been pressured – even demonised – to stop investing in new production. The ethical case is that they need to help ween the world off oil (more urgent is to cut coal use, but that’s a different problem). The economic case is that it makes no sense to invest in producing more of something for which the market is, or soon will be, shrinking.

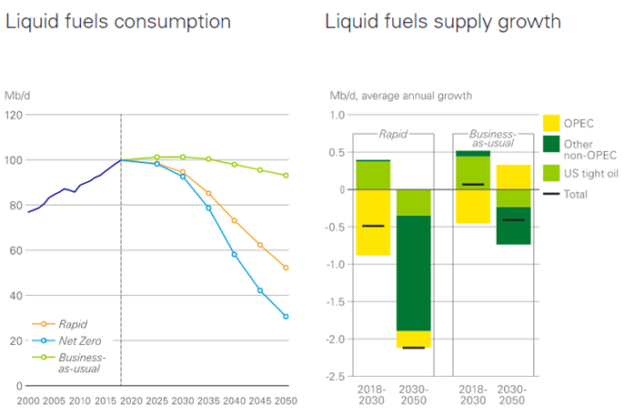

Views differ on just when peak oil demand will come. In 2020 BP brought forward its forecast of peak demand to…2020 (see diagram below) assuming either its “rapid” or net zero scenarios.

Even in a rapid decarbonisation scenario there will be a need for some oil and gas production, but existing reserves will supply most of that. There may be an economic case for one or two companies to do some new investment, particularly if all their competitors were to stop. But in practice most of that investment will probably be done by the national oil companies such as Aramco, which have the lowest cost reserves and which will be the last oil companies to operate, after all the private companies have ceased production.

“Energy” includes both oil and electricity, but they’re different businesses

So if you’re a major oil and gas company, what do you do? The obvious thing seems to be invest in the new energy sources which are displacing oil and gas demand. This means electricity generation and, possibly, hydrogen production, though the latter depends on decisions by governments, and scientific opinion remains divided on the merits and feasibility of a hydrogen economy. (Another option is carbon capture technology, but the business case for that is unclear at present).

Oil and gas and electricity are often lumped under the term “energy”, but they are very different industries. In their upstream business (exploration and production) the big oil companies have a number of key skills, such as geological knowledge, project management (often in hostile environments), managing large scale capital spending and dealing with political risk.

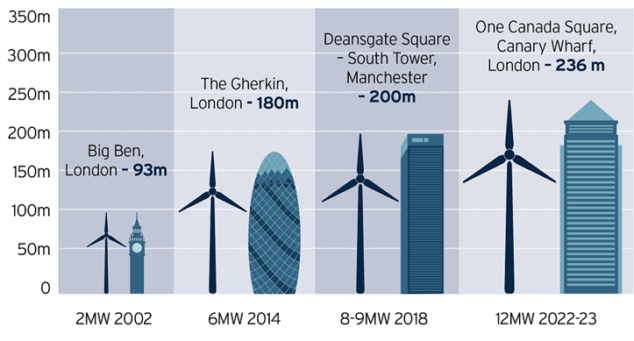

Electricity generation projects are generally much smaller than upstream oil and gas, and even when they reach the multi-billion dollar scale, are best thought of as modular. For example the Dogger Bank windfarms projects in the North Sea will be the largest offshore wind project so far, amounting to some £9bn ($11bn). That’s pretty big money for any industry. It’s a series of projects on the low lying part of the North Sea called the Dogger Bank, the name coming from a Danish word for fishing boats (it used to be a good place to catch fish before the North Sea was over-fished).

The total power capacity of the projects will amount to 3,600MW, which is about 5% of UK electricity demand. But each turbine is only 12MW. I say “only”, but these are enormous structures, about the height of the Canary Wharf tower (see graphic below), and a remarkable engineering achievement. In principle, a windfarm can be expanded indefinitely by adding more turbines, subject to space, transmission capacity and so on.

But the construction of big offshore wind farms, like the building of large solar power installations, is not something that the big oil and gas companies really know much about or have any particular expertise in. The technology is completely different from what they’re used to, and although some of their engineering skills are doubtless transferable, it’s not that related to their original business.

Diversification is risky

Of course they can buy their way into the business, and thereby acquire the skills. But so can anybody – the question is, does this amount to a sensible use of their shareholders’ funds?

Financial economists have a pretty strong view that a mature business should return cash to shareholders and let them decided how to deploy it in new, growing businesses. This is not just an article of faith; diversified conglomerates, having been fashionable in the 1960s when it was claimed that disciplined financial management at the core could act as a kind of internal capital market, fell out of favour and were broken up in the 1980s and 1990s. It makes sense that management are usually good at one or two things (at best) and risk making mistakes if they try to move into unrelated activities.

Perhaps the key example is the diversification of cash-rich tobacco companies, which bought into food, hospitality and other sectors. One famous example of how this approach was dramatically reversed was the famous takeover and break up of RJR Nabisco, told in the book “Barbarians at the Gate“, still one of the great books about finance. RJ Reynolds was the tobacco arm, Nabisco was a food company. Investors argued it made little sense for these completely different businesses to be owned and run by the same company. Better instead to let the shareholder have shares in two separate companies and make their own decisions about portfolios.

Since then many diversified companies have streamlined their activities through spin offs, or risk having a hostile takeover do it for them.

Of course electricity is not “unrelated” but the word energy should not obscure the big challenges of moving into what is quite a different business. One risk to shareholders is that oil companies over-pay for renewable energy assets, depressing returns for their own shareholders but also for those of existing renewable companies. Some investors raised their eyebrows at the recent result of the UK’s latest offshore wind auctions, in which BP entered the market for the first time, winning jointly with German utility EnBW permission for 3,000MW of capacity. Rival Royal Dutch Shell reportedly said its offer was “nowhere close” to BP’s. Of course that might be either sour grapes or a difference of strategic value. French oil company Total was also a successful bidder, in partnership with Macquarie, an experienced infrastructure investor who should know what they’re doing.

But managing decline is hard

One counter-argument to the argument that companies should just return cash to shareholders is that it is hard to manage a company in steady long term decline. It’s difficult to attract ambitious, talented young people, it’s hard to motivate the existing staff. People tend to be motivated by a goal, or a vision, and a vision of gradually shutting down production, cleaning up the abandoned sites and steadily seeing everything decline is not a motivating vision, even though it’s very important that this be done well.

The electric utility sector has seen attempts to deal with this dilemma by creating new divisions for renewable energy that are eventually spun off, leaving a mature and declining fossil fuel generating arm. Perhaps that’s what the big oil companies will eventually do.

*

UPDATE

McKinsey has an interesting article on what oil & gas companies should do. Among the insights are that: “The best-performing low-carbon companies are now achieving comparable returns over their (lower) cost of capital versus their oil and gas peers. The spread over the cost of capital for low-carbon energies such as renewables can be 200 to 250 basis points higher relative to oil and gas players.”

Jon

Hello Simon,

Great post. Another potential area to look at could be “downstream operations”. I would guess there would be more synergies between the existing fuel retail operations of oil majors and “new world with mostly electric cars”. Of course, we can debate whether a major investment into wind farms is needed to achieve this.

Simon Taylor

Yes, there could be synergies in the retail side, since petrol stations can be converted to be charging points. But there’s not much value in that side of the business.

Jon

Yes, especially from a ROCE perspective, that is the “inconvenient truth” 🙂

Simon Taylor

I’m not sure what you mean. Upstream expected returns have typically been 15-20%. Offshore wind is closer to 5%, though of course the risks are also much lower. A lot of analysts seem to think that BP paid a high price in the recent UK offshore wind auction, implying even lower returns.