Most economist agree on the causes of the repeated crises of the Eurozone but that explanation is not the one that many governments, and the European Commission, want you to believe.

*

The problems of the Eurozone – bank failures, sovereign debt crises and bailouts and above all a protracted recession and mass unemployment – have acquired various different “narratives”. In the orthodox one, which the European Commission and some governments (chiefly that of Germany) espouse, the root of the problem was too much borrowing by governments. On top of that, many governments have failed to reform their economies in the way that Germany did in the early 2000s (the Hartz IV reforms). The solution, logically, is to constrain state borrowing in future, along with some technical changes to the Eurozone system.

But this orthodoxy is mostly wrong, so the solution is also wrong. Apart from Greece, which does conform to the stereotype, the other Euro countries that got into trouble had low state borrowing ahead of the crisis, lower than Germany.

An excellent new report from the Centre for Economic Policy Research clearly explains the path from a widely varying group of countries before the Euro, through a period of remarkable interest convergence during the early Euro days, to the sequence of crises that threatened to explode the single currency. Their narrative commands widespread support (economists are encouraged to sign up to say so). And the analysis is consistent with a huge amount of scholarship, plus excellent research from economists at the IMF (as distinct from the IMF official view, which is closely allied to the orthodoxy, though it appears to be diverging).

The story boils down to a new version of an old theme in international macroeconomics: the “sudden stop“. This means a situation when a country has been receiving large amounts of external (foreign-supplied) capital, which encourages a country to make investments and forces it to simultaneously run a balance of payments current account deficit. This has happened many times, mainly to emerging economies (e.g. Latin America in the 1980s, South East Asia in the 1990s). The “stop” is an abrupt end to the external finance, usually accompanies by a reversal of funds. This forces the borrowing economy into a sharp recession because the funding for investment (and possibly consumption) has been turned off. Companies go bust, unemployment rises and tax receipts fall, all very quickly and in a way that is extremely difficult for the government to cope with. The government, whatever its former financial position, will inevitably suffer a big fall in income and probably a rise in spending (depending on how generous the welfare system is). Soon it’s in debt, possibly a lot of debt. The country may no longer be able to pay for essential imports such as oil and the deteriorating economy simply confirms foreign investors in their view that the country is risky, so interest rates rise, making the country even more depressed and financially damaged. Eventually the IMF becomes the only source of new funds and it offers a bailout package, the price of which is sharp cuts in welfare spending and government investment.

The point about a sudden stop is that it’s very hard to deal with and it’s largely a private sector matter; it is foreign private investors who switch from optimism to fear, sometimes in a matter of days or even hours. Once a government faces a sudden stop it’s in serious trouble. It may have encouraged or welcomed the earlier inflows of foreign capital. But to some extent those inflows were externally determined, as foreign investors from banks, mutual funds and pension funds all sought good investment returns. International financial imbalances (some countries running current account deficits and others running surpluses) are normal and can be healthy, depending on what the foreign funding is used for. But when they abruptly unwind, that process can be devastating to the former deficit countries.

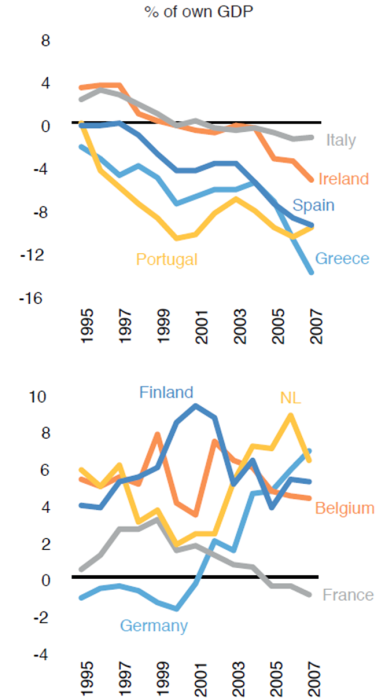

This is what happened in the Eurozone. But the difference from the usual emerging economy story was that the capital inflows which suddenly stopped were largely within the Eurozone itself, chiefly from the north to the south of the region. This chart shows the countries running current account surpluses and deficits on their balance of payments, expressed as a percentage of each country’s GDP. Running a surplus means that the country is exporting capital, that the country has a surplus of savings relative to investment and that surplus is being sent abroad. A deficit means the opposite.

The countries that later got into trouble were those that were running deficits, meaning they were importing capital from the surplus countries. Note that the figures are expressed relative to each country’s GDP so Germany’s surplus was in absolute terms very large, given that it has the largest GDP in the Eurozone area.

So “northern” Europe was lending to “southern” Europe. The lending was mainly by banks, which treated all Eurozone countries as having equally low credit risk, as evidenced by the fact that interest rates converged almost exactly across the whole region. One day, essentially the day that the new Greek government revealed in October 2009 that Greek government borrowing had been understated (the figures had been deliberately distorted by the previous government), lenders suddenly reconsidered that assumption and stopped lending. The abrupt stop in lending caused real estate bubbles in Spain and Ireland to collapse, local banks to look shaky and government finances to suddenly turn sour. These events confirmed the northern lenders in their views and they withdrew credit even more, thus reinforcing the downward spiral.

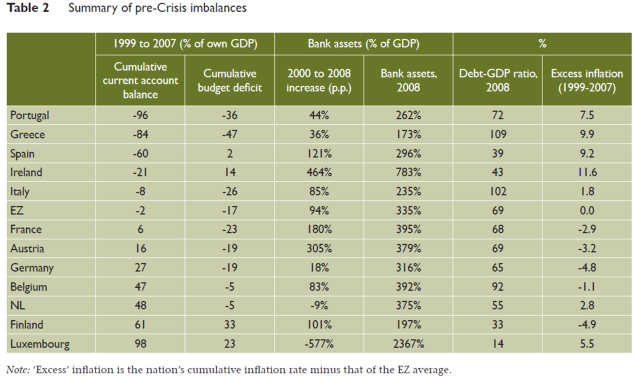

The orthodox narrative blames governments in Ireland, Spain and Portugal for borrowing too much. But their subsequently high debt came as a result of the crisis, not before it. This table from the report shows that Ireland and Spain had far lower government debt than Germany in 2008. It was the collapse of the Spanish construction sector and the nationalisation by the Irish government of its (private sector) banks’ debts that put each country into trouble. Each had previously been running a surplus. Portugal did have somewhat higher government debt to start with but much less than Greece or of Italy (which didn’t ever get to the point of needing a bailout).

The Eurozone crisis unfolded in several acts from 2010. The report doesn’t say that Ireland and Spain were blameless. Each country had an unsustainable property boom which generated high but somewhat illusory tax receipts to the government. But those booms were funded by banks in France and Germany. The first set of Eurozone bailouts essentially bailed out those banks at the expense of the people of Ireland and Spain. The fact that both countries are now showing signs of economic recovery (five years later) should not be taken to mean that all is well. Half a generation of young people is unemployed, many with permanently damaged economic prospects. And support for the EU has been badly shaken, possibly for good.

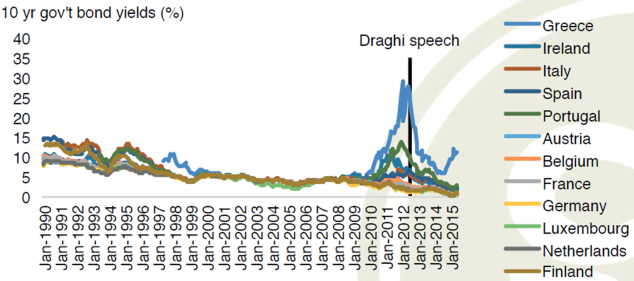

The crisis threatened to destroy the Euro. Having started treating all Eurozone countries as more or less the same, lenders started to differentiate between them, as shown by the divergence of government bond yields in the next chart. It was only when the head of the European Central Bank Mario Draghi made his famous speech about doing whatever it takes to protect the Euro as a whole that yields began to converge again. But it would be most unwise to assume that that the underlying weakness of the Eurozone has been fixed.

The report is clearly, carefully and calmly written but economists are widely angry with the European Commission and with the politicians of Germany and France for forcing the single currency, a largely political project, on Europe. Germany now calls for rules to be enforced on government borrowing. Yet the first two countries to break the original rules of the original Eurozone Growth and Stability Pact were France and Germany. It’s hardly surprising that many young European are now rather cynical about the European ideal and expressions of “solidarity”.

rjw

Thanks for the recommendation Simon. Really exceptionally clear paper and narrative, and very persuasive. I see you have not lost your touch for recommending good stuff (I am still grateful, even now, for you pointing us towards Jon Elster’s “Sour grapes” on some reading list, as an undergraduate, many year ago…….)

Simon Taylor

I’m pleased that my recommendations sometimes are helpful!

Shaocheng Yin

Thanks to Dear Director Simon bring us brilliant narratives on Euro Crisis. It is truly different angel of view to insight of this issue. It also creates me a lot of ripples of my thought pool.

True, the euro is in an unprecedented predicament distress. So many economists, scholars including Mr. Simon devote themselves in thinking of it, this means that Euro crisis is not only european problem, it, actually, involves you, me and everyone, it is our problem. The essence of the issue is the fate of Euro currency.

In fact,emergence of the Euro, both in practice and theory field, which is a brave exploration in the monetary history of mankind. It broke the boundary of national sovereignty, it is a self-challenge for the power and desire of printing money, since the birth of paper money(banknotes).

From John. Law(Edinburgh) and Mississippi Bubble to Isaac. Newton (England) and Gold Standard System; From John Maynard Keynes (Cambridge) and the General Theory of Employment, Interest and Money to Adam Smith(Scottish again) and “invisible hand”, then to American Robert A. Mundell (the Father of the Euro) and “analysis of optimum currency areas”, monetary unit had staggered through a journey with hardships.

Overall, the Euro crisis are telling us that there is a long journey for us to find a way out for monetary distress.