The foreign exchange reserves held by governments, having risen for over a decade, have recently fallen. This is mainly because they are being used, as intended, to protect against turbulence in financial markets that would otherwise hurt the developing economies.

*

Foreign reserves are assets held by governments as a safety net against abrupt changes in foreign exchange markets. Most rich countries don’t have to worry about such things because their currencies change relatively slowly and they have mature, sophisticated economies which can adjust reasonably painlessly to exchange rate changes. But emerging and developing economies can suffer substantial damage from large and sudden changes in exchange rates arising from either a change in foreign investor sentiment or as a side effect of monetary policy in the rich countries, chiefly the US but also Japan.

What are foreign reserves?

Any country can have foreign assets, which means claims on non-residents i.e. people from other countries. A UK citizen who brings home a €10 note from holiday in France owns a foreign asset. Companies which export earn foreign exchange and if they retain it they also have foreign assets. Alternatively they can sell it on the foreign exchange market for their home currency. A country which runs a balance of payments current account surplus (loosely speaking, it exports more than it imports) will automatically acquire claims on the countries it exports to, which means it builds foreign assets.

Countries also have foreign liabilities. Most obviously domestic residents may borrow abroad, perhaps to take advantage of lower interest rates (but that can be dangerous). Also a country acquires foreign liabilities from an inflow of investment from abroad. A flow of foreign investment into a country, for example to buy a company, means an inflow of foreign currency but then that foreign owner has a claim on the country’s assets. So foreign investment gives rise to foreign liabilities.

The sum of foreign assets and liabilities is the net foreign asset position. This is mostly made up of private assets and liabilities, at least in rich countries, where the state doesn’t intervene in the foreign exchange markets and the vast majority of foreign transactions arise from the private sector (the main exceptions being international aid and payments for international organisations such as the IMF and World Bank).

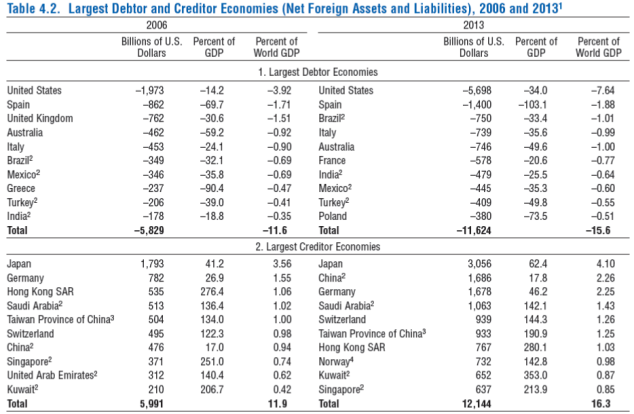

Here is the net foreign asset position of the largest net debtor and creditor countries.

Notice that the US is the largest debtor and Japan the largest creditor, in absolute terms. But Spain is a far larger debtor relative to its economy (103% of GDP). These figures, which are somewhat imprecise, capture the total of all claims between foreign and domestic residents for each country, including private and public debt. So for the US, the indebtedness reflects the very large holdings by foreigners (about half the total outstanding) of US government bonds. These foreigners (which include both private investors and foreign central banks and sovereign wealth funds) have chosen to buy US government bonds because they’re liquid and low risk.

Partially offsetting the US debts are the holdings of US investors in foreign equities, bonds, real estate and direct investment (Walmart’s ownership of ASDA in the UK, Ford’s ownership of car plants in Europe). These assets pay, on average, a higher return to the US than the cost of servicing the country’s foreign debts. So the US has a net debtor position but still earns a net positive flow of income on its foreign assets and liabilities. This could of course change if interest rates were to rise.

Only a part of a country’s net foreign assets is classified as foreign reserves. These are assets which are owned and controlled by the government or a central bank, which can be used to intervene in foreign exchange markets. They are equivalent to the stock of ready cash held by a person who wants to have some emergency funds, just in case, or to the stock of liquid assets that commercial banks hold in case all of their depositors ask to take their money out of the bank at once.

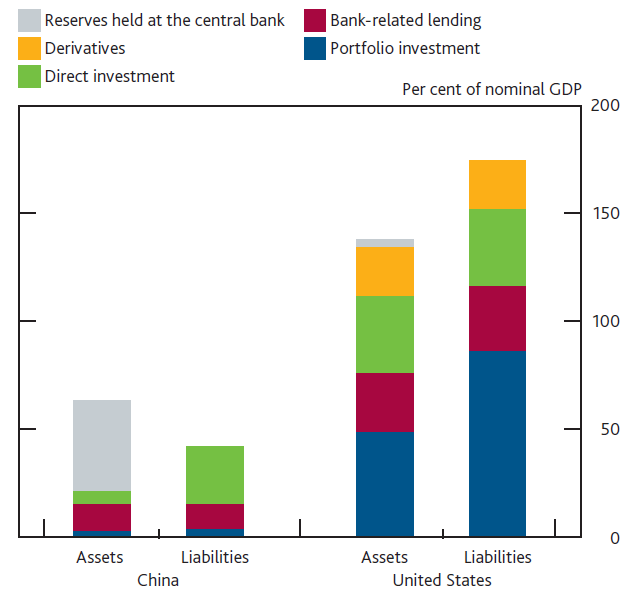

The relation of foreign reserves to total foreign assets and liabilities is illustrated in this chart from the Bank of England, which shows the total net foreign asset position for China and for the US as of 2012.

The chart shows firstly that China has greater foreign assets than liabilities while, as we’ve already found, the US has the opposite. The US has far larger gross assets and liabilities relative to its economy, because it is much more financially open and integrated into the world. By contrast China is heavily integrated into world trade but not world finance.

The silver bar represents those foreign assets which are classified as foreign reserves. For the US these are quite small. The US simply doesn’t hold many foreign reserves (though it does hold a lot of gold, which could in principle be sold for foreign exchange, though not very quickly without crashing the gold price). The US has large foreign assets in the form of portfolio investment (holdings by US residents of foreign equities and bonds) plus bank-held assets (loans to foreigners) and foreign direct investment. But the US has even larger liabilities in respect of portfolio investment: it is the world’s favourite destination for foreigners to buy shares and bonds. The US also has a lot of inward foreign direct investment, which counts as a foreign liability.

China has much lower gross foreign assets and liabilities but has a positive net balance. This is entirely and dramatically made up of foreign reserves. China’s portfolio assets and liabilities are very small because capital controls restrict the ability of foreigners to buy Chinese financial assets (though this is gradually changing) and of Chinese to buy foreign assets. In direct investment China is a large net debtor, because it has received a lot of foreign investment in the last twenty years, which has been encouraged by the government and has contributed to the growth and modernisation of the Chinese economy. (It’s important not to think that because foreign direct investment is a “liability” that it is somehow a bad thing.)

But China’s overall foreign balance is dominated by the foreign reserves owned by the central bank and managed by SAFE (the State Administration of Foreign Exchange).

What sort of assets are foreign reserves?

To be useful as reserves, foreign assets need to be liquid (quickly and cheaply converted in money) and safe (so they don’t lose their value just when you need them). The perfect asset is US government bonds, which trade in a deep, liquid market and enjoy the creditworthiness of the world’s largest economy. A close substitute is the bonds issued by the government-owned housing finance institutions Fannie Mae and Freddie Mac. Although both companies had to be bailed out and de facto nationalised (the official status is “conservatorship”) by the US government during the financial crisis, they are seen as entirely backed by the US government and so they are almost as creditworthy as conventional US government debt.

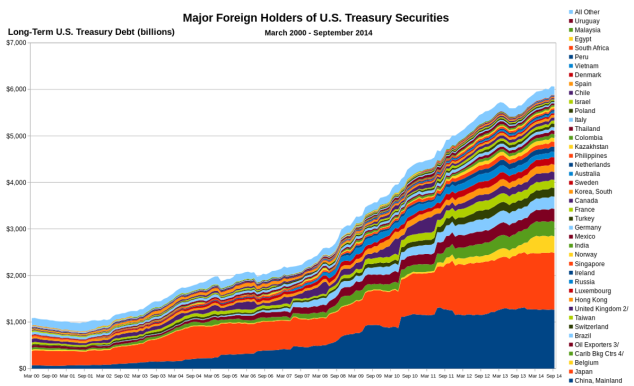

Unsurprisingly then, most countries hold a large part of their foreign reserves in US dollar assets, much of which is government debt. The chart below shows the big rise in foreign holders of US long term debt (they also own short term debt) from the early 2000s, accelerating from 2009, when the US budget deficit was rising fast but foreign appetite to buy it was rising equally fast.

How and why do countries build reserves?

Reverting to our comparison of an individual who feels it prudent to hold spare cash in case of unexpected trouble, that person can only get the cash by saving some of their income. Equally countries must save some of their national income to build reserves. More accurately they must set aside some of the income from foreigners that they receive, either from exports or from foreign investment in their country. Foreign reserves represent a form of wealth or purchasing power. Every dollar held in reserves could have been spent on buying something from the US. So it’s a form of saving.

In practice, central banks build reserves by intervening in the foreign exchange markets and here there is a difference between China and most other reserve-holding emerging economies. China for many years wanted to hold down its exchange rate, to keep the RMB competitive against the dollar. A Chinese exporting company, receiving dollars from a US importer, would want to convert them into RMB. In a purely market driven foreign exchange market the company would sell the dollars to buy RMB. That would slightly push up the value of the RMB and slightly push down the value of the dollar. When China was generating a large trade surplus AND receiving large foreign direct investment flows the RMB would have faced considerable upward pressure. But the Chinese central bank forced the exporting companies to sell the dollars to its reserves fund, thereby removing the downward selling pressure on the dollar. The dollar/RMB exchange rate was therefore stronger (in favour of the dollar) than it would otherwise have been, making Chinese manufacturers more competitive and US companies less competitive, which naturally raised tensions in trade talks between the two countries. (That policy has now stopped and the RMB is more-or-less market determined. If anything, the central bank is now intervening to support the RMB value, which has been under pressure from capital flows out of China)

The side effect of the Chinese central bank intervention was to build foreign reserves that peaked at $4 trillion in 2014 and were about $3.5 trillion in late 2015.

Other countries wanted to build their reserves following the Asian financial crisis of 1997. A key feature of that crisis was a sudden reversal of the large but short term flows of foreign funds into south east Asia economies such as Thailand, Malaysia and Indonesia, causing enormous economic and political turmoil. Many governments then decided to build their reserves to provide a buffer against any such future instability. They also intervened in the foreign exchange market, keeping their currencies lower than they would otherwise be and pulling foreign exchange out of the market into central bank reserves. These countries, unlike China, were targeting higher reserves, with the weaker exchange rate being a means to that end.

But in both cases the building of reserves meant, necessarily, that many developing economies were running balance of payments surpluses (an equivalent way of saying that they were increasing their national savings relative to their national investment). That meant necessarily that some other country had to run a deficit, and that was mainly the US. So the large US deficits of the 2000s (which peaked just ahead of the financial crisis – and that is not a coincidence) were a necessary counterpart to the surpluses of many other countries.

The tide may have turned

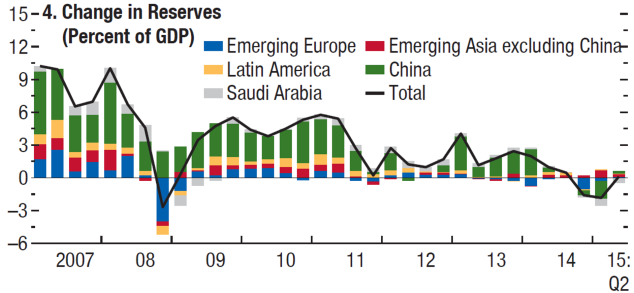

In 2015 the long standing pattern of global reserves rising appears to have halted and even reversed. The chart below is from the latest IMF World Economic Outlook, published in October 2015. It shows how reserves growth, which was around 9% of global GDP in 2007 has fallen to zero or even negative in the first half of 2015. We know that reserves fell in the third quarter of 2015 too.

Note that the biggest part of the reserve growth since 2007 is the green bar, China. A smaller part came from other emerging economies in Asia and Latin America and some from Saudi Arabia. In 2015 three things have happened to push the reserves down:

- China’s economic slowdown has led to capital flight out of China to the rest of the world, despite exchange controls

- Brazil and Russia have suffered recessions and large exchange rate falls as a result of China’s falling demand for their exports

- Oil exporters including Russia and Saudi Arabia have suffered a large fall in the oil price which has cut their income and led them to use some of their reserves to fill the gap.

China’s capital flight is probably temporary, so long as the economy stabilises and there is no repeat of the stock market panic of 2015. But China is unlikely to grow its reserves in future. Some of the foreign reserves will be used to fund China’s planned overseas infrastructure investment (including the “one belt, one road” programme).

Brazil, Russia and Saudi Arabia face a more difficult and lasting problem, assuming that commodity prices remain below their previous highs for some time which is the current consensus. They can draw on their reserves for a while, which is precisely what they are for, to provide a temporary smoothing mechanism and to buy time for more profound economic adjustment. None of the countries will want to see their reserves fall too far, for fear that they will become vulnerable to a collapse of confidence and a self-reinforcing spiral of capital flight and plunging currencies.

Abdulai Nyei

What an excellent piece on foreign reserves. Thanks a lot Simon!