Macroeconomics is a complicated subject but it’s possible to understand quite a lot about the key questions in macro, and some of the policy challenges, by considering a few key concepts. This blog gives the elements of what ties macroeconomics to finance. I’ll apply these concepts in a follow-up blog to try to explain why there is some cause for concern about long term weakness in the world economy.

*

All economic transactions can be classified into two equations: i) the current account; and ii) the capital account. We use these to separate different types of economic decisions in a way that provides helpful information about the economy and financial system.

The current account says that people have a single decision about what to do with their income: either consume it or save it. Consumption, to economists, means spending on things that are relatively short term in nature such as services, food and rent. Spending on longer term assets such as cars or houses counts as investment (*).

So the current account is:

Y – C = S

Y stands for income because the letter I is conventionally used for investment.

This simple equation invites us to ask, why do people save. The main motives for saving are to smooth their consumption over their lifetime (especially for retirement) and to have reserves against bad luck. A lot of economic analysis and measurement goes into understanding what determines consumption, which accounts for about 75% of a developed economy’s GDP. Understanding changes in saving behaviour is therefore critical to both short term economic forecasting and to understanding the longer term path of the economy.

The capital account says that any savings made (there may be none) are available to fund investment. If the person or company has access to a financial system then they can also borrow to fund investment beyond what their savings will support. In general, if savings and investment are different, there must be either net lending or net borrowing.

The capital account is:

S – I = net lending (which can be positive or negative).

Note that any gap between S and I must give rise to some sort of financial transaction, meaning a change in financial assets or liabilities. For example, if I save 100 out of my monthly income but do no investing, I have S = 100, I = 0 and net lending of 100. That could show up as 100 in the bank: I acquire a financial asset worth £100, which is the bank’s liability (they must give it to me if I ask for it).

If I saved £100 but wanted to buy a car for £1,000, I would take out a loan (most cars are bought on credit). I have net borrowing of £900, because I’ve got £100 in the bank but I’ve taken on a loan (a liability) of £1,000.

All loans or financing arise from a gap between S and I. For me to be able to borrow or lend, there must be somebody else (a bank, other financial institutions, a creditworthy relative) to take the other side of the deal. Even if I simply have £100 cash left over at the end of the month I have acquired a financial asset, namely a claim against the central bank, for whom the cash is technically a liability.

All of this is just classification; it doesn’t involve any particular theory about how people behave. It is also applicable at any level of economic aggregation, whether it’s the individual, a company, the household sector or the whole economy. And all lending and borrowing is bilateral: it can only happen between economic agents.

This means the sum of all net lending is zero. This is equivalent to saying that in the whole economy the sum of S cannot be different from the sum of I. If you think of S and I as real resources rather than financial items, it’s clear that it’s impossible for the entire economy to invest more than it has saved. The only resources available for investing are those which have not been consumed. In a very simple agricultural economy, of the type much studied by the classical economists of the eighteenth century, this could be thought of in terms of corn. Corn (in Europe this means wheat, barley, cereal crops, not maize as corn is known in the US) can either be eaten (consumed) or kept to provide seed for next year’s crop (invested). So the total amount of corn is pretty much total income and the village’s or farmer’s decision amounts to how much to eat versus how much to keep. It is impossible to both consume and invest the same corn; you must save some corn if you want to invest for next year’s crop. This is true for real economic resources in general, including in our complex economy.

Let’s take stock. For any part of the economy, people decide on how much to save and how much to invest, with any gap necessarily giving rise to a counterpart financial transaction. Finance is about the gaps between saving and investment (it’s also about managing risk but that’s another subject and less important in explaining the financial system). And for the economy as a whole saving and investment must balance so all financial transactions net out to zero: net lending must equal net borrowing.

International net lending: the balance of payments

We have to modify that last statement a little because most economies are open, meaning they trade with the rest of the world. This means that for a national economy total saving and investment need not balance because that country may be able to borrow from (or lend to) the rest of the world. Any such gap is called the balance of payments. We describe the balance in two ways: i) as the current account, which is roughly speaking the trade balance, reflecting any gap between resources entering the country and resources leaving; and ii) the capital account, which describes how that imbalance was financed. It is the same way of categorising economic transactions as we applied for households and firms in the domestic economy.

The logic of total S having to equal total I still applies but it now applies at the global level. Any one country may run a deficit or surplus on balance of payments (meaning that its total I either exceeds or is less than its total S, respectively). But for all countries taken together, deficits and surpluses must net out: there can be no lending without a borrower. This is equivalent to saying that all imports must be somebody else’s exports. If the world were a large farm, we could not globally invest any more corn than we had saved.

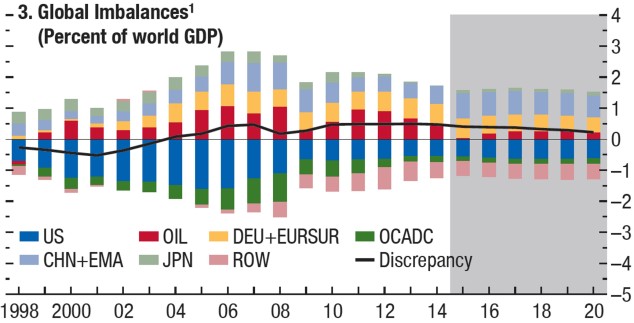

Once we understand that all countries (except perhaps North Korea) run deficits and surpluses, which must sum to zero, we can ask the question, what does the actual pattern of deficits and surpluses look like? And does it look in any way worrying? The chart below shows these surpluses and deficits grouped by the major economies, expressed as a percentage of global GDP. The logic of every deficit being matched by some other country’s surplus means that in any year the height of the bars above the line (surpluses) should exactly match the bars below the line (deficits). But imperfect data (including a large amount of illegal economic activity) mean there is a discrepancy shown by the black line. But the diagram still shows reasonably clearly the pattern of international lending and borrowing over nearly 20 years, both in terms of total scale (the height or depth of the bars each year) and the countries in surplus or deficit.

EMA is emerging Asian economies. DEU is Germany. EURSUR is the other surplus Eurozone economies. OCADC means other current account deficit countries. ROW is the rest of the world.

Interpreting this diagram gives us a lot to think about. Note that the picture of surpluses and deficits is dominated by the dark blue bars representing the US (a persistent debtor). The countries funding the US deficit vary somewhat over time. In the late 1990s the main lender was Japan (JPN). In the 2000s it was China and Emerging Asia which became the largest lender to the US. In some years the oil producing countries also lent but their surplus rises and falls with the oil price and in 1998 was actually a deficit. In recent years the yellow bar, representing the surplus nations of the Eurozone (chiefly Germany) have become larger.

The overall scale of lending and borrowing peaked in 2007, at the time of the financial crisis. This is no coincidence. The ease with which the US could borrow in the early 2000s (meaning lower interest rates than would otherwise have been the case) was a contributing factor to the unsustainable household credit boom in the US, mainly used to invest in real estate. The subsequent fall in international deficits and surpluses reflects the US recession and the abrupt increase in saving by US households, combined with an even sharper fall in real estate investment. This meant the US overall deficit fell in 2009.

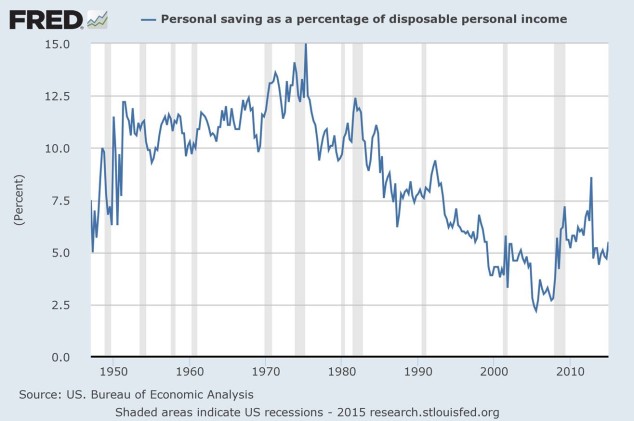

The US household savings rate decline: an important part of the picture

The chart below shows the long term fall in US personal sector saving as a proportion of disposable income, which was one cause of rising US international borrowing up until 2008. It also shows the temporary rise in US household saving caused by the financial crisis and the sharp fall in house prices, which made many households suddenly feel less wealthy and less optimistic about the future, two things that typically influence saving decisions. Explaining the long term savings decline is not at all straightforward but is essential to understanding how the US economy can grow sustainably in future.

The global financial imbalances have been lower since the crisis and the IMF forecasts (in its World Economic Outlook) that they will stabilise at lower levels. There is nothing wrong with international financing by one country of another but the scale and pattern of the financing matter, just as they do in domestic lending. Too much debt risks creating a bubble followed by a crisis in repaying the debt, something that predicted by a number of analysts watching the US for several years (so far they have been wrong).

This framework is based on the national accounting ideas I started with above. It treats borrowing and lending symmetrically. It therefore should remind us that if a country has borrowed too much then other countries must have lent it too much. Criticism of high consumption and investment in the US during the run up to crisis should be matched with criticism of those who willingly funded that spending.

This blog has shown how we can get quite quickly to a position of asking the right questions about international financing simply by knowing a little national accounting and classifying economic transactions into current and capital account. It is all about measuring what has happened. Ignoring data problems, actual investment and actual saving must be the same. But problems can arise when economic agents intend to save and invest in ways that are not compatible Since there is only a finite amount of corn to be either consumed or invested, any inconsistent plans must be reconciled somehow, including by changes in exchange rates and in GDP. The next post will examine the question of whether the world faces a persistent imbalance between intended saving and investment, which risks being “resolved” by slow growth and low employment: the secular stagnation thesis.

Notes

(*) All spending by consumers is classified as consumption in the national accounts but part of it is classifed as spending on consumer durables (e.g. washing machines, cars and other long lasting goods) which are, in effect, investment. Consumer durable spending behaves somewhat like business investment spending, being somewhat sensitive to interest rates and confidence about the future as well as typically being financed through lending, rather than out of income.

The IMF has a helpful short guide to GDP here. It gives more information about current account balance of payments imbalances here and the question of whether countries should liberalise the capital account of the balance of payments here.

Leave a Reply