Major world historical events such as the financial crisis that swept much of the world in 2007-09 typically have multiple causes. In 2014 there was an outpouring of new books about the causes of the First World War which started a century before. Historians continue to disagree about why the nations of Europe went to war and it’s likely that future historians will add new interpretations of the causes of the US-originated financial crisis that started in 2007 and reached its peak in late 2008. New books are still appearing about the great depression of the 1930s, which afflicted the US far worse than what is now informally known as the “great recession” which followed the 2007-08 crisis, challenging some of the previous orthodoxy (Barry Eichengreen’s latest book “Hall of Mirrors” is an excellent and readable contribution).

A new piece of research from the Federal Reserve Bank of New York adds to our understanding of the recent crisis by putting the growth of mortgage credit to US households firmly at the centre of events. Everyone agrees that it was the rise in US house prices that was the cause of the subsequent crash, made far worse by the shadow banking system of interconnected but unregulated financial institutions. But there are competing “narratives” as to how far the underlying cause of the housing boom was the Fed’s low interest rate policy or the government’s longstanding support of credit to lower income households. Those who want to see government as the source of all evil emphasise both of these explanations, though they have been fairly convincingly refuted.

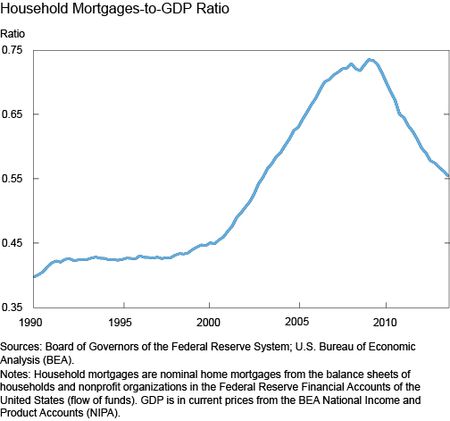

The FRBNY concludes that house prices rose because of additional mortgage lending brought about by financial innovation (securitisation and tranched credit) plus a rise in financial inflows from outside the US. What needs to be explained is the exceptional rise in mortgage lending to households, which surged relative to GDP (see this figure).

One explanation that has been widely accepted is that lenders made loans on weaker or lower collateral, consistent with the view that sub-prime borrowers (those with a poor credit record, ineligible for normal mortgages) were the main part of this rise in borrowing. But that is inconsistent with data showing that credit rose more or less in tandem with the underlying housing values, until they started falling in 2006. There were undoubtedly more poor quality borrowers but in aggregage the growth of lending was matched by the growth of the houses against which the mortgages were made.

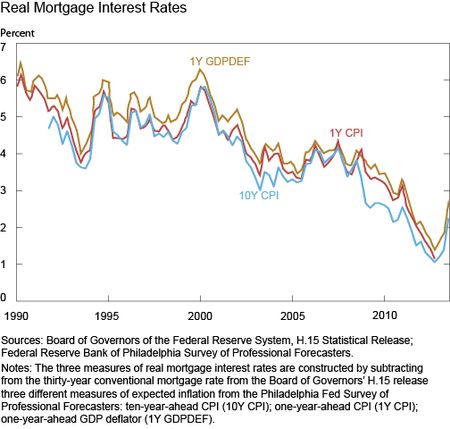

Also, lower collateral requirements and generally more lax lending standards would have triggered a rise in credit demand from those previously denied access to the market. That should have pushed up interest rates on borrowing (a rise in demand for a given supply) but on the contrary interest rates continued to fall right through the period. The chart below shows three different estimates of the real interest rate on mortgage borrowing, calculated by taking the nominal rate on 30 year mortgage borrowing and subtracting three different measure of inflation one year later. The steady downward trend in real long term borrowing rates is more consistent with a rise in credit supply than with a rise in credit demand, all else being equal.

It was the supply of credit, not demand

That suggests that the underlying cause was not on the demand side but the supply side – a rise in the supply of mortgage credit which pushed interest rates down even as the volume of mortgage lending was rising at an unprecedented rate. Where did that new supply come from? There were two reinforcing sources.

First “the pooling and tranching of mortgages into mortgage-backed securities (MBS) played a central role in loosening lending constraints through several channels.” The main reason for this was that tranching – the financial restructuring of middle quality loans into a mix of high quality and low quality through collateralised debt obligation (CDOs) – allowed the creation of new AAA-rated securities, for which there was a great demand. That demand came from financial institutions such as pension funds and insurance companies seeking good quality credit risk but a better yield than was available on US government debt, the main source of AAA securities. Corporate bonds rated AAA had become very scarce since the shareholder value revolution of the 1990s led to companies borrowing more to boost the value of their after-tax earnings, a result of interest payments on debt being tax deductible, unlike dividend payments. Many institutional investors can only buy AAA securities and were desperate to find better yields. So the creation of CDOs and other tranched credit vehicles brought a new source of institutional savings into mortgages which previously had not been available.

A secondary effect of the securitisation was “regulatory arbitrage”. Banks which hold mortgage loans on their balance sheets must allocate an amount of equity capital to reflect the risk that they default. By shifting those mortgages off their balance sheet into securities instead the banks were free to allocate that equity to new mortgage lending, on which they charged a fee, then securitised the loans again and so on, creating a new mortgage-origination supply, so long as there were willing buyers of the AAA CDO securities which were ultimately created.

The second cause of the rising availability of US mortgage credit was the increasing flows of foreign funds into US financial assets, including US federal debt and securities issued by the federal housing agencies Fannie Mae and Freddie Mac. This inflow, which was largely a result of balance of payments surpluses in Asia, particularly China, led interest rates to be lower in the US than they would otherwise have been. Note that the government/central bank investors in the US typically didn’t buy the AAA mortgage securities but they made the general price of such securities lower than they would have otherwise been by reducing the interest rate paid by the US government, which is the benchmark for all other borrowing, including mortgages. So Asian buyers of US federal government bonds made mortgage borrowing cheaper in general. The lower interest rate on government debt also encouraged more institutional private sector buying of the CDO securities, which offered a higher yield than government bonds. Foreign private sector buyers from the US, Germany and Japan did buy these CDO securities, helping to spread the damage when they defaulted or fell in value but the Chinese and Japanese governments generally didn’t buy them and suffered no losses as a result, other than the damage from the global economic recession caused by the financial crisis.

Conclusion

The FRBNY analysis is not surprising but it helps to focus the analysis of what went wrong. Most financial crises result from excessive lending, usually by banks, to some part of the economy. Historically this has included domestic real estate, commercial real estate, agriculture, commodities and emerging market governments. Each time there is a reason why the banks believe that it is safe to lend more than before and each time they learn that it wasn’t. The biggest equity bubble in recent years was the technology, telecom and media stock surge in the late 1990s. This led to some trillions of dollars of losses to investors but it wasn’t funded by a surge in credit so it did relatively little macroeconomic harm. The lesson is that we must find ways to discipline the level of debt.

Samir Dave

Hi Simon Sir,

It is nicely explaining the trends & analysis,

If you could also include Dos & Dont’s for avoiding such scenarios as well,

Wish a Great Day!

Thanks!

Best Regards,

Samir Dave

India

+91 9824476998

Adam Haeems

Hi Simon. Very interesting read on the financial crisis of 2007/2008. What is particularly surprising is the household mortgages-to-GDP ratio over the period, clearly that level of lending was unsustainable.

I believe ‘moral hazard’ also had a part to play in the crisis with regards to ‘regulatory arbitrage’. These securitised products created distance between the originators of the loans and the ultimate investor who bore the risk of default. This allowed originators to reduce screening standards of new borrowers in order to increase loan volumes along with their fees/commissions, as they bore none of the default risk.

It can also be argued that a lack of financial literacy among the ‘subprime market’ had a part to play in the increased borrowing. Many of this subprime market were sold mortgages with ‘teaser rates’ via new mortgage products such as Adjustable-Rate Mortgages (ARM). Deregulation in the mortgage industry at the time did away with restrictions that imposed a ceiling on the interest rates lending institutions could charge, allowing for innovation in the mortgage market resulting in many new products targeted at the subprime market. Many of these borrowers had little understanding of interest rates, and that their mortgage payments could dramatically increase after the introductory teaser rate.

Great blog Simon, I’ve become a regular visitor. I’m also due to start the MFin at JBS Cambridge this September and am looking forward to it immensely.

Regards,

Adam Haeems

Abdulai Nyei

Hi Simon,

I found this article very interesting.The global finaicial crisis, experience in 2007-09 can not be made clearer than this.

Infact, I am a regular visitor on your sit here, I read almost all your articles. My wife and I name our Dog Sooty as well. 🙂

Good job,

Abdulai Nyei