CDOs – collateralised debt obligations – were widely seen as the main villain of the financial crisis. CDO issuance peaked in 2007, collapsed in 2008 and is now gradually recovering. Should we be worried?

*

The latest Bank for International Settlements Quarterly Review has an article about the slow revival of CDOs. The CDO was at the heart of much that went wrong in the global financial crisis. In 2007 most people even on Wall Street and in the City couldn’t tell you what a CDO was. By 2009 every newspaper was describing these complex products to their bewildered and angry readers.

A collateralised debt obligation is a special purpose vehicle (a company set up to repackage and restructure cashflows) used in securitisation – the conversion of a set of cashflows from loans into a set of securities. Securitisation of US mortgage loans started in the 1970s and became a mainstream feature of the US mortgage market by the 1980s. A package of mortgage loans by banks would be combined, through a special purpose vehicle, into mortgage backed securities – MBS. These could be sold to any credit investor round the world and were very popular, because US mortgages rarely defaulted and it was a way for say Japanese investors to diversify their investments into the world’s largest capital market.

A CDO takes the securitisation a stage further. Starting in the 1980s, a package of underlying assets, which could be corporate loans or MBS, is transformed into a set of new securities, of varying risk, known as tranches. Tranches vary from low risk (supposedly) to high risk. The top tranche is the first to be paid out of the cashflows generated by the underlying assets and is the least likely to be hurt by any default. So that tranche has the lowest credit risk and pays the lowest interest rate. Lower tranches become proportionately more exposed to the risk of default and so pay a higher interest rate.

There was, and remains, a shortage of high quality (i.e. low default risk) securities suitable to be held by insurance companies and pension funds, which are often required to stick to low risk investments. The top credit rating of AAA is now quite rare in the corporate bond world because most companies are run for the benefit of equity shareholders, who have little interest in keeping a company so safe that its bonds are rated AAA.

CDOs allowed the manufacture of AAA rated securities to an almost unlimited degree. So long as the credit rating agencies gave the CDO securities the top rating, there was a ready demand from them from institutional investors round the world seeking the credit quality of the US government (or at least very nearly) but with a slightly higher yield than that paid on Treasury bonds. Strong demand for the securities meant that CDOs were very profitable and they duly increased enormously as investment banks sought mortgage backed securities as fuel. That in turn spurred mortgage brokers and banks to originate new mortgages. Households were able to borrow at less than before. Everybody seemed to gain.

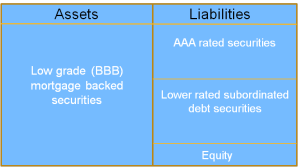

A CDO can use any financial asset as its “fuel”. But the most popular type in the last few years before the financial crisis was one that took low quality MBS, those rated BBB, which were too risky to be held by some institutional investors. By repackaging them into a form where the CDO could issue AAA rated securities, investment banks could manufacture more of what the market wanted – high quality securities. Here is a CDO balance sheet. As with most balance sheets it’s easiest to interpret the assets as uses of funds and the liabilities as sources. So the CDO buys MBS by selling securities to investors. The company (usually an investment bank) which “sponsors” (sets up) the CDO must put some equity in, though even that can be sold to other investors, such as hedge funds who are happy to take this higher risk investment.

The highly profitable process of turning mortgages into MBS and then MBS into CDOs depended on mortgages remaining low risk. Since everybody with a good credit record pretty much had a mortgage by 2003, the only way to expand demand was by offering loans to those without a good record – the sub-prime borrowers. So the MBS that the CDOs invested in were in turn being backed increasingly by lower quality mortgages. There was therefore an increase in leverage in the underlying assets (mortgages) and then additional leverage in the financial engineering that created the AAA securities issued by CDOs. The rest is history, as US house prices accelerated upwards, then fell far more than most people had ever imagined, trashing the credit ratings and taking CDO security valuations with them.

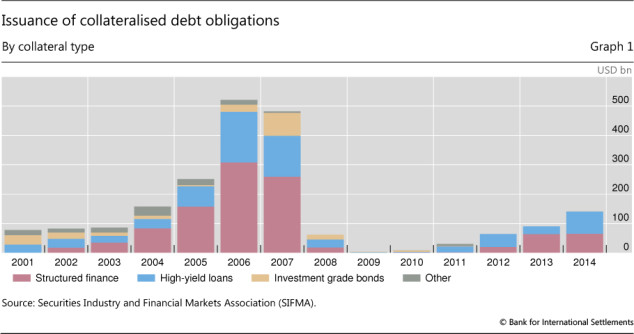

As the BIS diagram shows, CDO issuance stopped completely in 2009 and has only started to recover, slowly, in 2013-14.

So somebody is creating CDOs and somebody else is buying their securities. The US housing market is in much healthier shape than before the crisis and there is more regulation in place to prevent loans being made to people who can only afford to repay them if the house value rises, which defines a speculative investment. So the risks of buying CDO-issued securities may be lower than before. The BIS report analyses some of the mistakes in earlier CDO structuring that meant they were more risky than they seemed and were downgraded proportionately more than the underlying assets. Perhaps today’s investors are more sophisticated and understand what they’re buying, rather than just relying on a credit rating agency opinion which was itself often flawed. Let’s hope so.

Dan

The problem this time around is leveraged loans (Libor +250-350 bps) packaged up as CLOs. Beware: there is a maturity wall coming up in 2017-2018. If libor were to normalize back to 200-300 bps, weak credits face rollover risk. Restructuring activity will pick up.