Money can mean physical cash, or the funds in a bank account or the flows of short term funding used by government and companies. No wonder finance can be confusing.

*

Finance is a subject bedevilled by jargon – words, phrases and acronyms that are barriers to understanding the relatively simple things that actually go on in much of the financial world. Some of this is a side effect of experts talking to each other, using convenient shorthand. Some is perhaps deliberately intended to keep out the riff raff to preserve the prestige, and incomes, of those who “speak” finance.

But we also make the subject more difficult by using the same word with different meanings. This is usually because many finance words have an everyday use that isn’t exactly the same as the professional meaning. “Capital”, “investment”, “savings” all have confusingly varied and different meanings. And so does the word money.

Money can mean the physical currency – notes and coins – that you have in your pocket. It can also mean more generally a person’s wealth – “How much money does he have?” doesn’t mean the stock of notes he owns but his overall purchasing power or wealth. That’s the meaning of “money” in these references:

“For the love of money is the root of all evil” First Epistle to Timothy, New Testament, King James Bible

“Money money money, it’s not funny, it’s a rich man’s world” Money, Money, Money, ABBA

“The best things in life are free/But you can keep ’em for the birds and bees;/Now give me money, that’s what I want” Money (That’s What I Want), Barrett Strong

To an economist money means anything that has the functions of money, which are: i) a generally accepted means of payment; ii) a store of wealth; and ii) a unit of account. This obviously includes physical currency but it also covers the much larger stock of funds in bank accounts. You can store your wealth in a bank account (it’s safe but not going to make much of a return). You can certainly count it, just like cash. And it can be used to pay for things, either by being converted into currency through an ATM or by electronic transfer.

The magic of bank money

What makes the bank account money seem special is that banks make it. They literally invent it out of nothing. Students, when they first grasp this, are both impressed and somewhat appalled. A common reaction is, so it’s not real? But if you can pay for things – real things – with your bank account and you can take it out as cash, then it is surely quite real. But it’s also entirely electronic – it exists only as a number in a computer file.

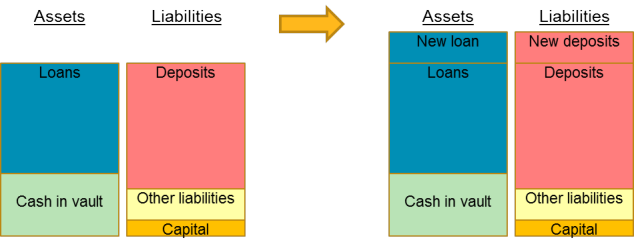

This is rather perplexing. But it may be less so when we learn that banks don’t invent money and spend it at will. On the contrary, all the money that banks create in the form of new bank account deposits is a liability, it belongs to their customers, not to the bank. Each time the bank makes a new loan (which is an asset for the bank) the bank simultaneously creates a new bank deposit balance (which is a liability for the bank) – see the diagram below.

The bank is no better or worse off after the simultaneous creation of a loan and new money. And neither is the customer. Each has acquired exactly offsetting assets and liabilities. The bank later makes a profit because the cost of making the new funds is close to zero but the bank receives interest on the loan. The person taking out the loan, the customer, can do something useful with the loan (buy a car or holiday) which is presumably worth the cost of the interest. So both the bank and customer are better off as a result of the loan and the new money being created. That’s why banks are (sometimes) useful.

Monetarism

Back in the late 1970s and early 1980s there was a brief period when some economists, central banks and governments believed that controlling the volume or stock of money in the economy was necessary and sufficient for macroeconomic policy, a movement known as monetarism. Using some rather simplistic assumptions about how the economy worked, a number of clever people believed that it was possible and desirable for central banks such as the Fed, Bundesbank and Bank of England to control the money supply. This, they thought, would achieve control of inflation without unnecessary turbulence in the wider economy.

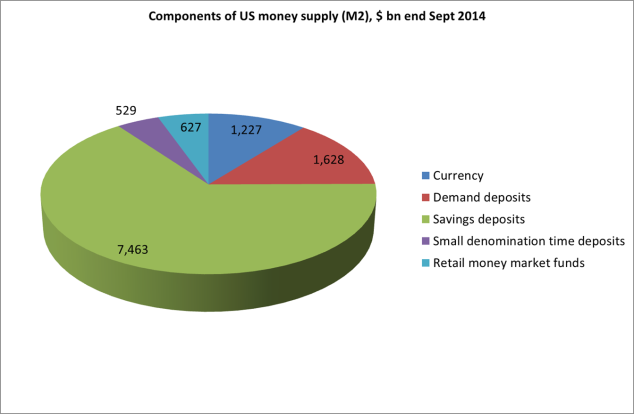

There is a long and detailed history to be written about the fiasco that monetarism became. In short, central banks abandoned it as it became clear that there was no longer, if there ever had been, a stable relationship between the money supply and inflation(*). Nearly all central banks now set the interest rate and let the money supply adjust passively. Part of the problem was defining what IS the money supply? You can try to control only what you can measure and you can measure only what you can define. There is narrow money: pure notes and coin currency. We can add to that the current account balances in banks that are available on demand to get a measure of broad money. But we can also add savings accounts which can be converted very quickly and easily into current accounts. And what about money market funds, which are very close in practice to current accounts? You get quite different numbers depending on your definition. This diagram shows the components of one measure of broad money in the US, called M2.

The very term money supply is misleading if it implies that the central bank is in control of the creation of money, because it isn’t – the great majority of money in an advanced economy is supplied/created by commercial banks, as we saw above. Central banks issue only the physical notes and coin, a fast diminishing fraction of the total money supply. And even that supply is largely a passive response to demand by the general public.

The money markets

“Money” is therefore an ambiguous term. But we aren’t finished yet. There is another use of the word in finance, which is to refer to the money markets. Confusingly, this has nothing to do with currency or bank accounts. It refers instead to the needs of companies and of governments for short term financing, meaning funds of less than a year’s maturity. There is a vast and complex network of supply and demand for such funds, which arise from the fact that most organisations have seasonal differences in their cash income and cash spending, even if they’re in balance over the year as a whole. So the government gets lots of funds in during the period when taxes are paid but needs to raise funds the rest of the year.

The various ways in which these funds are raised include certificates of deposit (CDs), commercial paper, repos, Treasury bills and Eurodollars. Trillions of dollars in the US alone flow through these channels between companies and households who have spare funds they want to put into safe, interest bearing assets and other companies, plus the government, which want to raise temporary funds. Quite why this is referred to as the money market is unclear, though it’s convenient. It is in contrast to the markets for funds for longer than a year which are collectively known as the capital markets.

So the word money gets used rather a lot of finance and there is always room for confusion. Whatever the context though, nobody ever seems to doubt that they want more of it.

*

“Money, so they say,/is the root of all evil today./But if you ask for a rise it’s no surprise that they’re/giving none away” Money, Pink Floyd

NOTES

(*) Fed Chairman Alan Greenspan told Congress in 1993: “The historical relationships between money and income, and between money and the price level have largely broken down, depriving the aggregates of much of their usefulness as guides to policy. At least for the time being, M2 has been downgraded as a reliable indicator of financial conditions in the economy, and no single variable has yet been identified to take its place.”

Leave a Reply