In the wake of the financial crisis, which showed the surprisingly fragile state of conventional western banks, people have looked for alternative ways of delivering financial services, especially credit. The IMF recently compared two types of banking that may offer lessons: cooperative banks and Islamic banking.

Cooperative banks are owned by their depositors. They may engage in a wide range of banking activities but are typically focused on retail lending. Credit unions, which originated in the US and are still common there, are a form of cooperative bank. When I worked at the World Bank I had to join their credit union to get paid. Cooperative banks are not entirely free of problems but they have had a much lower rate of failure than commercial banks and they are not systemically risky, though this is partly owing to their small share of the banking market.

Islamic finance refers to lending and other financial services that are conducted under Sharia law. Sharia is the “moral code and religious law” of Islam. In a few countries it is also the national law. In others individuals may wish to use only financial products judged to be consistent with Sharia.

The chief feature of Islamic finance is a prohibition on receiving interest on loans, because it is said to be unjust to be paid when taking no risk. This is the same position taken by the Catholic Church in Europe during the Middle Ages under its prohibition on usury, which it argued was a mortal sin. One reason for the stereotype of the Jewish moneylender (e.g. Shylock in Shakespeare’s The Merchant of Venice was because Jews were not blocked by their faith from lending, at least to non-Jews. Unscrupulous European monarchs periodically attacked Jews for lending as a pretext for taking their money (e.g. Edward I’s Statute of the Jewry in England in 1275). But Jewish lending was economically valuable so it reappeared later.

Despite active prosecution by the Church of bankers who broke the usury law, credit availability expanded in the 12th and 13th centuries, laying the foundations for the early capitalist era of trade based on the Italian city states of Venice and Florence. Bankers found ways to disguise loans by introducing an element of risk, which then justified an interest payment, or by making them futures transactions. The Church gradually lost the battle against usury and although it is still against Canon Law, the ban has not been enforced for centuries. English King Henry VIII, having broken with the Roman Catholic Church in the 1530s, allowed lending at interest in a law of 1545. Protestant (non-Catholic) Christian countries like the Netherlands and England led financial development and innovation from that time onwards and the Italian cities went into decline (there were other reasons too of course).

The moral condemnation of interest shifted from any interest at all to apparently excessive or unjust interest, more than could reasonably be justified by the risk or cost of lending. This is of course subjective and a matter of endless dispute (see recent press outrage about “payday lending” in the UK for example).

The ban on interest in Sharia has not been lifted or changed, as it is so clearly stated in the Qu’ran. So what is widely called Islamic finance has evolved in the second half of the twentieth century, driven by the rise of a new middle class which wanted mortgages and business loans that were Sharia-compliant. The key to making the transaction Sharia-compliant is that the bank providing finance must take risk. So a mortgage may be organised in such a way that the bank owns the house and allows the “borrower” to buy it gradually through periodic payments. In the event that the customer doesn’t default, the substance of the cashflows may look very similar to a conventional mortgage loan but the risk element is essential.

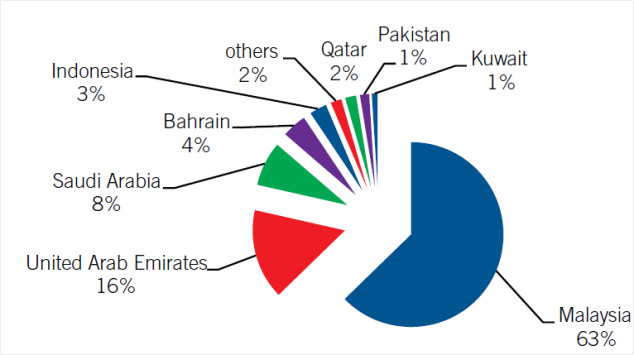

Islamic retail finance is potentially a huge market – there are around 1.8 billion Muslims. But not all wish to stick to Sharia law. So in practice Islamic finance is concentrated in the Gulf region and in Malaysia. Indonesia and India, which are where the two largest concentrations of Muslims live, are not yet significant markets.

Islamic finance embraces government and corporate fund raising too. Sukuk are Islamic financial certificates that substitute for bonds. In 2012 $144 bn of Sukuk were issued according to the Global Islamic Finance Report. About 70% of Sukuk issuance is by sovereigns, with Malaysia the main issuer. Saudi Arabia launched its first sovereign Sukuk issue in 2012. The rest is mainly used in infrastructure investment in the Middle East.

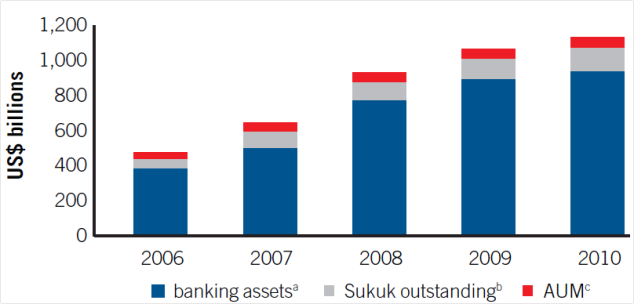

The same source estimates total Islamic finance assets at the end of 2012 as $1.6 trillion, a growth of 20% on 2011. This is a large number but global financial assets are estimated by McKinsey at $225 trillion. The IMF estimates worldwide total credit union assets at $1.6 trillion in 2011. So Islamic finance remains a relatively small part of the total financial system, though it is one of the fastest growing.

Islamic finance and the MFin

The Cambridge Master of Finance degree (MFin) tries to cover all the important areas of finance. Islamic finance is still something of a niche and of interest mainly to those working in Muslim countries or countries with large and prosperous Muslim populations (the UK is increasingly one of these). But the principles are interesting and potentially applicable to other countries and economic systems, so we have an annual guest lecture on Islamic finance by an expert practitioner from the Middle East.

CJBS has hosted events on Islamic finance from time to time. An enterprising Malaysian MBA student arranged a seminar three years ago, for example. And CJBS’s Executive Education arm is running the first of a series of courses on Islamic Finance in Cambridge in November. My colleague Dr Kamal Munir talks about Islamic finance and the course in this video.

Further reading

A World Bank analysis of Islamic financing.

A case study of Islamic financing of a container port.

The growth of the middle class is a global phenomenon and this article by Vali Nasr of Johns Hopkins University argues it is central to understanding the Arab Spring as well as the growth of Islamic finance.

KS

Simon,

This idea of risk-free lending seems ridiculous when you start thinking about it from the risk-reward perspective. There is no free lunch in this world. The payments are there but the state has to bear them. This scheme is possible only in those countries where religious rules are more important than the free market economy. I do not believe that the countries which have free market economy could possibly afford such banking schemes which are nothing more but very costly solutions.

Is it really worth teaching such rules to the future market makers at the business school which strives for some world recognition?

KS

Simon Taylor

Islamic finance is not subsidised by the state. And Islamic principles more generally are not incompatible with markets and trade. From the tenth to twelfth centuries the Fatimid Caliphate was the world’s largest de facto free trade zone, spanning the Middle East and North Africa, cemented by Islam, the lingua franca of Arabic and political stability. Western “too big to fail” banks are subsidised by the state, which insures their creditors without compensation for taxpayers. Islamic banks ought to be less likely to fail, so there is no a priori reason for thinking they are in some way less sustainable or socially valuable than non-Islamic banks. From the MFin curriculum point of view it seems reasonable to spend a few hours out of a one year programme to teach students about a system of finance potentially applicable to 1.8 billion people.

mba in islamic finance

Overall article is awesome i completely agree with the writer but islamic finance is not small anymore

Agapito

Thank you for a very nice article… if you want something such as Certified Islamic Banker you can check http://www.arabworldinstitute.com for more of financial courses they offer that is inclined in islamic rules.