Despite persistently low inflation since the global financial crisis, there are plenty of commentators and investors who predict inflation will rise. They base this on i) the huge increase in central bank balance sheets arising from unconventional monetary policy “quantitative easing” and ii) the argument that the only way to deal with the large levels of public debt in most of these countries is to “inflate” it away. It’s now some four years since the British and American central banks expanded their balance sheets but inflation and inflationary expectations still show no sign of jumping in the way the inflation pessimists predicted So let’s look at the second argument.

Public debt, meaning the debt of the public sector, is high and rising in most rich countries. It’s especially and uniquely high in Japan but in many other countries it is at or beyond the 90% of GDP threshold that many economists believe triggers slower economic growth (1). So how can the debt problem be fixed? There are three solutions.

Three ways to cut debt to GDP ratios

First is to run low budget deficits or even surpluses. This entails higher taxes or spending cuts or both. Politically these are unattractive policies, especially when there is evidence that such “austerity” may reduce economic growth and cause the debt/GDP problem to get even worse, an argument applicable to Spain and Greece and possibly the UK.

Second, the government can default. It can simply refuse to repay some or all of the debt. Or it can change the repayment terms to reduce the real burden, as has been done in Greece, where maturities have been stretched out to give the government much longer to pay. No rich country would choose this except as a last resort, as it means either shutting down access to future borrowing (eg look at Argentina since its default in 2001) or at best higher interest payments. Greece is only getting help because it is obviously unable to pay and the Eurozone governments prefer Greece to somehow stay in the Euro.

Third is higher price inflation that erodes the real value of the debt. This is a “soft” default, since the debt holders suffer some loss. But it is not an outright repudiation. And there are some clear historic precedents.

The main example, which is studied in chapter 3 of the IMF’s October 2012 World Economic Outlook, is the rapid fall in US debt to GDP in the ten years following the Second World War. In 1946 the US faced up to the price of massive war spending in the form of public debt of 120% of GDP. By 1951 it was down to 75%, despite the cost of the Korean War which started in 1950. The IMF calculates that higher inflation contributed about half of this fall, the rest coming from economic growth and a primary (pre-interest cost) budget surplus.

So it’s not surprising that people might think the US in particular might see inflation as a relatively painless way to deal with the public debt problem. But whatever the government might want to do (and I see no evidence that the Treasury or the Fed or their UK equivalents are even contemplating this policy) it is most unlikely that this policy would work this time.

The problem is that investors are now much wiser to the risk of inflation. In the 1950s and again in the 1970s, inflation was unexpected, or as economists prefer to say, unanticipated. And crucially many investors had nowhere to hide. The large institutional investors which own the majority of government debt could not in those days put their money abroad or buy inflation-linked bonds, which didn’t exist. High inflation that robbed them of the real value of their investment was a form of financial repression, which is depended now on exchange controls and other regulations that prevented investors taking their money abroad.

Now, investors are constantly on the alert for rising inflation and run global portfolios which allow them to shift huge amounts of money into other countries and other assets at short notice. So a sudden increase in inflation would reduce the real value of the debt somewhat but the need to finance new deficits would mean that investors would demand far higher interest rates as compensation for anticipated inflation – plus a premium for the greater uncertainty about inflation.

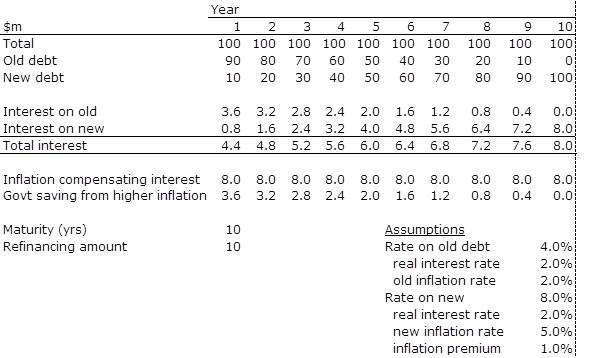

A numerical example to show how quickly the benefits are eroded

Consider an example. The government has $100bn of outstanding debt with an average maturity of ten years. So each year it has to refinance $10bn of the debt. Assume there is no budget deficit, so the government has no additional debt to finance. The interest rate on the old debt is 4% and price inflation is constant at 2%, for a real interest rate of 2%, which is a reasonable estimate of the long term real rate. So the annual interest bill is $4bn.

Each year the government must find $4bn to pay investors. $2bn of this is the real interest payment and $2bn is compensation to investors for inflation. The real value of the debt stock is gradually falling because it is denominated in nominal terms – each bond is $100 and that amount will fall due at some point, which is eroded in real terms because inflation is 2% so the real purchasing power of $100 is gradually falling. But the fall in the real burden of the nominal stock of debt is exactly matched by the extra interest paid to investors.

Now imagine that somehow the government or the central bank engineers an immediate rise in inflation to 5% and keeps it there. The real value of the debt is now falling at a faster rate. Instead of being halved in 36 years, it is now going to be halved in just over 14 years (this is the rule of 72 – divide any compound growth rate into 72 to find out how long it takes for the amount to halve or double). An extra three percentage points or $3m a year of interest would be needed for investors to be compensated for this. But the interest payments on the existing debt are fixed at 4%. Investors are screwed on this debt.

But on any new debt, including the refinancing of the old debt as it falls due, the investors will want at least the extra 3% and will probably demand a bit more for fear that more sudden jumps in inflation will take place. Let’s assume they are willing to buy new debt at an interest rate of 8% – 2% real + 5% inflation + 1% inflation risk premium. So when the next tranche of $10bn of maturing old debt comes up for refinancing the government will have to pay 8% on it – $8bn of interest.

So the government benefits through the saving on (real) interest on old debt but faces the cost of higher interest on any new debt. I assumed that the government had no budget deficit. But if it does and if that deficit is large, as at present, then the extra interest cost of refinancing the old debt plus selling the new debt will be much higher than before. And if the maturity of the debt is shorter then more debt has to be refinanced at the new higher rate. So, the benefit may turn out to be not that big when the costs are considered. By the time all of the old debt has matured, 10 years in this case, the interest cost benefit has disappeared.

This tells us that the ideal situation for a government thinking of inflating away its debt is one where the debt has a long maturity – preferably an infinite one, like UK consol perpetual bonds – and where there is no budget deficit to finance. By contrast the worst conditions are when the existing debt has a short maturity (the US actually has an average maturity of just over five years) and when there is a large budget deficit to finance. The US deficit is currently at 7% but forecast by the independent Congressional Budget Office to fall by 2015 to about 2.5% before rising again in the longer term as health and social security costs rise.

The benefit of inflating the debt would be higher if the public believed that inflation has only risen temporarily, in other words if investors were fooled. But although investors are not necessarily rational all the time, they are very unlikely to allow themselves to be fooled again over inflation, having suffered such large losses in the past. So it would be wise to expect than any increase in government/central bank inflation policy would be very quickly picked up by bond investors, whose required interest rates on new debt would jump accordingly.

Empirical estimates confirm it’s not a useful policy

Analysis done by Michael Krause and Stéphane Moyen of Deutsche Bundesbank (available here) confirms that only very high inflation would have much effect on the stock of US federal debt. They find that of the additional US public debt arising from the 2008/09 economic crisis (not the previous “normal” debt) “about a third is cumulatively inflated away after ten years if the inflation target is permanently raised by four percentage points.” A temporary change in the inflation rate of four percent for four years has only a negligible effect. And in this latter case the credibility damage done to monetary policy would last for years to come. Krause and Moyen don’t calculate that cost (because they assume money is neutral economically) but it could be substantial.

A recent report from RBS comes to similar conclusions. They estimate that the UK could reduce debt/GDP back to the pre-crisis level of below 50% through a period of 15% inflation for five years. No government would contemplate that unless the alternative was catastrophic. And no credible Governor of the Bank of England would acquiesce in such a policy.

This solution isn’t going to work and rational central banks and governments won’t even try it.

*

Note (1) The main source is Carmen Reinhart and Ken Rogoff (2010) “Growth in a Time of Debt” which can be accessed here. A related paper by the same authors with more historic detail is available here. Robert Shiller, among others, casts doubt on whether their 90% threshold is more than arbitrary. Yeva Nersisyan L. Randall Wray argue that Reinhart and Rogoff’s work isn’t relevant to the US, with its floating exchange rate and ability to borrow in its own currency. Japan, which has the same features, has over 200% public debt to GDP but so far hasn’t collapsed, though annual growth per working person has been only about 1.2% since the early 1990s (a lot better than pure stagnation of course). There is agreement that too much debt impedes growth but no consensus on whether there is a trigger level or if so, what that might be.

UPDATE May 2014

A much more sophisticated analysis confirms that inflation is unlikely to make much difference to US debt unless it’s at very high levels.

clemence ... (^^)

appreciate your kindness …. very invaluable opinion for specialists who have great concerns about “debt and inflation” (^^)