The fundamentals of global economic growth seem broadly positive but there are some reasons for caution, which can be understood through the savings-investment framework described in the previous blog. If savings are “too high” or investment “too low” then the equilibrium rate of interest that makes savings and investment equal may be negative. That means policy interest rates, which cannot practically be lower than zero, may not be able to fall far enough to e

*

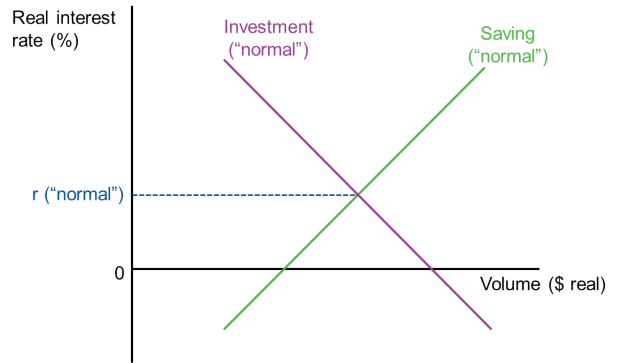

Savings and investment balance at the equilibrium rate of real interest

I argued in a previous blog that total savings and total investment must be equal. If we think of real economic resources, then any resources used for investment (to provide benefits in the future) can only come from not consuming all of the resources now, which is what we call saving. If all economic transactions are accurately classified as consumption or investment then we should find at the end of the year that aggregate saving equals aggregate investment. But this is only true for the world economy; any individual economy may have a surplus or deficit, which means that there is a counterpart deficit or surplus elsewhere in the world. A country can, in effect, “import” savings from other countries which are willing to lend to them.

We can radically simplify the world economic picture into a single diagram that shows savings and investment as functions of the rate of interest. Many things affect saving and investment decisions, some of which are insensitive to the rate of interest (the age structure of an economy is very important for saving, for example). But we should expect that broadly speaking savings increase if the rate of interest rises, because higher interest offers an incentive to defer consumption to the future (i.e. save). We should also expect that broadly speaking investment (spending on real assets that will generate future benefits) will decline as interest rates rise, because the interest rate is the cost of investing.

So (once again, we’re simplifying a lot here) we can plot global savings and investment as in the following diagram.

The savings and investment lines cross at a point which determines the global interest rate, labelled r (“normal”). At that rate of real interest, the overall desire for saving and desire for investing are in balance.

The natural rate of interest: full employment equilibrium

What we learned in the earlier blog post is that savings and investment must balance. But there are lots of different combinations of S and I that balance (*). An old but important concept in economics is the natural rate of interest, the rate at which S equals I and there is full employment of resources in the economy (**). Full employment is a normal goal of economic policy. If S = I but there is unemployment of people and capital, then the economy is not healthy. In the 1930s British economist John Maynard Keynes argued, against the conventional view, that savings could equal investment, meaning we have an equilibrium, but with unemployment persisting indefinitely, meaning we get stuck in a depression.

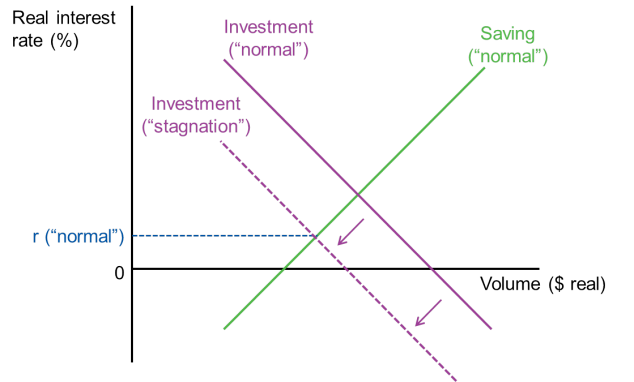

The diagram above shows S = I at a positive rate of interest. But what if the two lines only cross at a negative rate of interest? And how might this happen?

This diagram shows what would happen if there was a general fall in investment intentions. This could happen for a number of reasons, including a fall in confidence (equivalently a rise in risk aversion), a fall in expected future returns (perhaps caused by expectations of generally lower economic growth) or a fall in the intrinsic productivity of investment because of lower innovation. If this general fall in global investment intentions happens it will push down the equilibrium rate of interest. But as long as it’s still positive there is still a possible equilibrium of S = I at full employment. The pattern of economic activity would change but there would still be full employment.

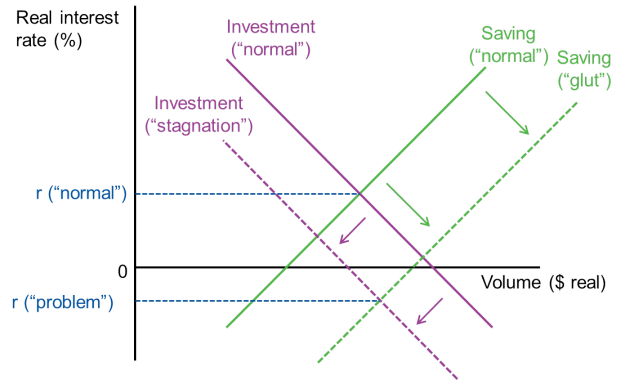

But what if at the same time there is also a rise in savings intentions? This could be caused by many things, including a rise in risk aversion (people worried about the future tend to save more, just in case), a change in government policies on welfare, especially pensions, and changes in the age structure (a rapidly ageing population is likely to save more in anticipation of retirement, especially if there are fewer young people to look after them than before).

If S rises and I falls we could face the situation in this diagram, where the equilibrium interest rate is negative. Recall that we are talking about real interest rates, the rates applicable to real resource decisions. But nominal interest rates, the ones we actually observe in financial markets, cannot normally go negative (there are some limited exceptions). So the problem is that the rate of interest needed to achieve full employment equilibrium of savings and investment is unattainable.

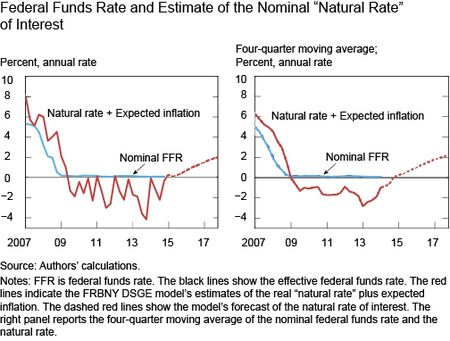

Some people believe that we have already been living through this situation. The Federal Reserve Bank of New York’s economists estimate that the “natural” real interest rate for the US has been negative in recent years (see chart). This is a fairly widely held view. Note that we can’t directly observe the natural rate of interest, only estimate it on the basis of imperfect models of what interest rate is needed to provide full employment. This chart shows the New York Fed’s recent estimate of the underlying natural rate of interest for the US, from a blog post called Why Are Interest Rates So Low?. The Fed has taken the real rate and added expected inflation to get the nominal natural rate of interest, so they can compare it with the actual nominal Fed Funds rate, the short term interest rate targeted by the Fed’s monetary policy (which has been close to zero since the financial crisis).

The NY Fed argues that the short term policy interest rate is low because the underlying natural rate is low (and possibly still negative). Fed policy is not causing globally low rates, it’s responding to them. But the NY Fed (and its view are broadly held by other major central banks) believes the real rate is rising back above zero to a more “normal” level. Many financial market practitioners disagree with this analysis, believing that low central bank rates are distorting financial markets. The Fed believes that it had no choice but to keep rates low because the natural rate, which is largely outside their influence, is low.

The problem for policy makers like central banks is that if the real (equilibrium full employment) rate of interest is negative but actual nominal policy interest rates can’t go negative then we face the risk of persistent unemployment and poor economic growth. Savings and investment will still balance, as they must, but not at full employment. Central banks in the US, UK, Europe and Japan used (and still use in the case of Europe) unconventional monetary policy (including quantitative easing) to try to stimulate the economy beyond a near-zero policy interest rate. The Fed, noting that the US economy is now growing reasonably fast and unemployment has fallen considerably, is confident that the problem has largely been fixed and nominal rates will soon rise.

Three versions of secular stagnation

But a more pessimistic view holds that the real interest rate, both in the US and globally, remains negative and could persistently stay that way. This is known as the secular stagnation thesis, though it comes in at least three different forms, depending on the reasons why S is expected to remain high, I to remain low, or both.

- developed economy private investment is persistently too low because CEOs are incentivised to maximise short term returns at the expense of long term investment; so companies are under-investing relative to what would make shareholders (and the wider economy) better off;

- investment is less productive than previously and likely to remain so, because technological innovation has slowed down; even if this hasn’t happened yet, it will happen in future because we lack general purpose innovations of the scale and importance of computing, electricity and the invention of modern chemistry, all of which fuelled decades of rapid growth in the past;

- savings are “too high” because several developing economies, but especially China, have ageing populations who are anxious and uncertain about how they’re going to provide for their retirement and for other forms of social spending like healthcare; they don’t trust the state to provide and the traditional solution of being looked after by children (or grandchildren) is neither workable (too few young people) nor popular with the young people themselves.

There are arguments for and against each of these propositions and corresponding policy suggestions. For example, we could try to change the CEO incentives, alter the tax system to encourage innovation, invest more in fundamental research (much of the research that powers the modern economy was funded by the US government), and urge the Chinese government to accelerate its plans for pension provision. Japan seems to putting its faith in robots to help manage its older citizens, which if successful might make retirement cheaper and possibly nicer for many otherwise isolated, lonely people.

Conclusion

The framework of a natural rate of interest which balances saving and investment at full employment is an old concept but which is helpful for thinking about national and global financial balances. It’s the framework that underpins most central banks’ policy decisions. There are ground for believing that global savings and investment behaviour are currently not compatible with a positive natural real rate of interest.

This is an important question about the long term potential of the world economy. The optimistic view is that the negative natural real interest rate is temporary, a hangover from the global financial crisis which is now beginning to correct. Optimists also argue that the internet of things, the extraordinary rise in cheap access to information across the world and the advance of medical science will all yield innovations quite big enough to keep investment profitably flowing.

But if savings and investment behaviour is stuck in a pattern that makes the natural rate negative then monetary policy cannot get us back to full employment and faster economic growth. Government action may then be needed.

A final way to combat the negative interest rate is for governments to mobilise (not necessarily to actually carry out) extra investment in projects to prevent and mitigate climate change. These carry an uncertain return but can be thought of as insurance against potentially disastrous outcomes. Climate change is by far the largest threat to long term economic growth and indeed to humanity in general. Other forms of state-sponsored investment such as China’s “one belt, one road” plans to build a high speed train network across Eurasia are to be welcomed too.

(*) Those who’ve studied economics will recognise that combinations of S and I that are equal are plotted as the IS curve in income and interest rate space. This is because S and I are themselves influenced by the level of national income. In the text above I’m abstracted from that to emphasise the long term structural relationship of S and I. Some would argue that there is no such structural relationship but the framework I’m describing is one shared by most central banks and mainstream economists.

(**) Narayana Kocherlakota, President of the Minneapolis Federal Reserve, refers to the “long run neutral rate of interest” but I think he means the same thing as the natural rate.

Further reading

Federal Reserve Bank of Richmond Calculating the Natural Rate of Interest

Federal Reserve Bank of San Francisco Economic Letter: Why So Slow? A Gradual Return for Interest Rates

Vox EU The equilibrium real funds rate: past, present and future

Analysis of whether the causes of low real rates will reverse by Tim Taylor in his blog

DDD

In your last post you used a simple formula that I could not disagree with: Income – Consumption = Saving.

What is interesting is that in your last post you didn’t use the $ sign in conjunction with that equation, whereas in the graphs here you do. The question that pops to mind is: where is the link to real currency, and what if that assumption is incorrect?

The Economist magazine has a wonderful unit of currency: “cost of a Big Mac”, which IMO is a lot closer to reality in your formulae than the $ sign that you use. I’d be interested to see how much of a problem is being masked by statisticians using “biased” currency valuations.

The value of the dollar, GBP, Yen, Renminbi, etc. is driven by sentiment and trust, not mathematical formulae. Most countries have similar profiles of 1% super-rich, 10% rich … 5% very poor. So why is a rich country considered rich, and a poor country considered poor?

Is there some hidden wealth “locked up” in the infrastructure of the UK that just doesn’t exist in a developing country? Is King’s College chapel the UK’s wealth (or maybe the monstrosity they are building near the station)? Is it the education system, or the economic cycles of the work that people do?

Probably not – it’s ultimately the exchange rate… and some strange imperceptible level of “Trust” in the developed countries’ economies.

So then what happens to your graphs if we remove the bias? Well, probably something really strange – we’d see that despite a huge and clear overvaluation, the $ is still doing really, really, really well. In the face of any form of common-sense, equation or explanation something is holding the developed world at a different level to the poorer countries.

Ironically, I think that your C value is now the problem (and ultimately IMO developed countries’ downfall). There just isn’t anything much that people aspire to buy any more, so Income equals Savings. Which surely must lead to an interesting collapse of some kind in the near future…

Simon Taylor

All the diagrams refer to real variables so the currency sign is just to help distinguish the volume from the price (interest rate). I’m not sure what you mean by biased valuations. Currency values in markets are certainly affected by sentiment in the short run but more likely to reflect underlying economic forces in the longer run. A nation’s wealth consists of anything that gives value to its citizens, including fine architecture and institutional capital such as a tradition of trying to educate well. Measuring those things is very hard of course. But the value of the rule of law and societal trust are probably more important than physical assets. Germany and Japan lost much of their physical wealth by the end of World War 2 but within a generation were among the world’s leading economies. I don’t think there’s much evidence that people have run out of things they want to buy yet. The increasingly unequal distribution of income may be a problem for aggregate consumption though, as richer people tend to spend a lower fraction of their income.